Despite the selloff over the last two months, the broader markets are positive through three quarters of 2023. U.S., international, and emerging market indexes declined in August and September.

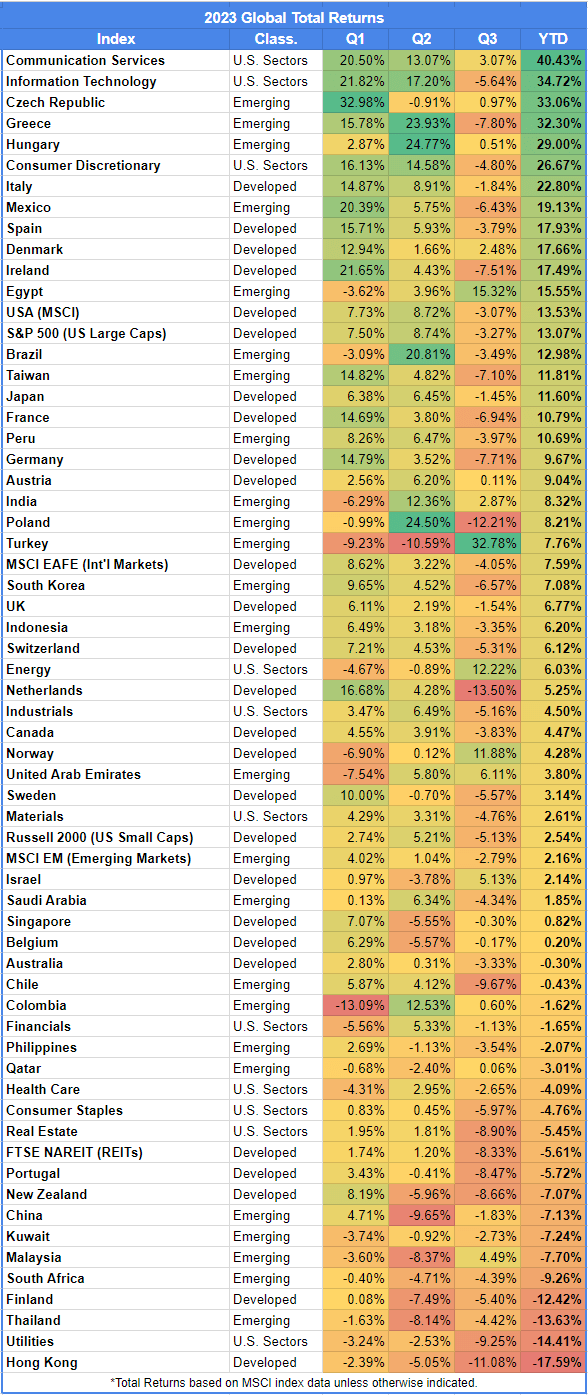

The S&P 500 finished the third quarter with a 13.1% return year to date, down from 16.9% at the end of the second quarter. The international market index closed the quarter at 7.6%, down from 12.1% in Q2. Emerging markets dropped to 2.2% at the end of Q3, down from 5.1% in Q2.

Both REITs and high-yield bonds (Agg index) turned negative for 2023, due to third-quarter declines. But cash (a basket of short-term T-Bills) and high-yield bonds buck the trend with gains over the last three months. High-yield bonds rose to 6% on the year, while cash rose to 3.7% year to date.

A note before getting to the 2023 numbers. The asset class, sector, international markets, and emerging market return quilts are up-to-date through the third quarter. Hit the links for each one.

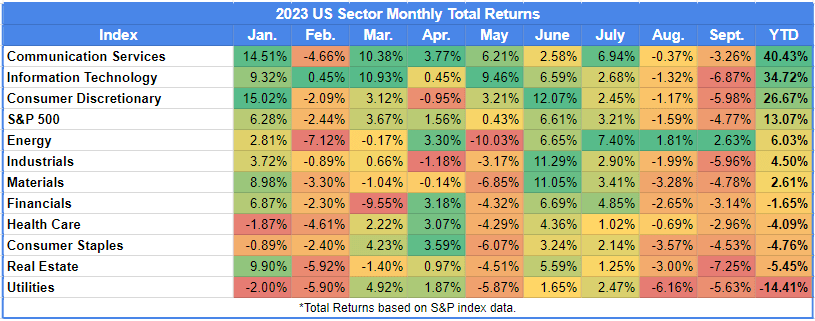

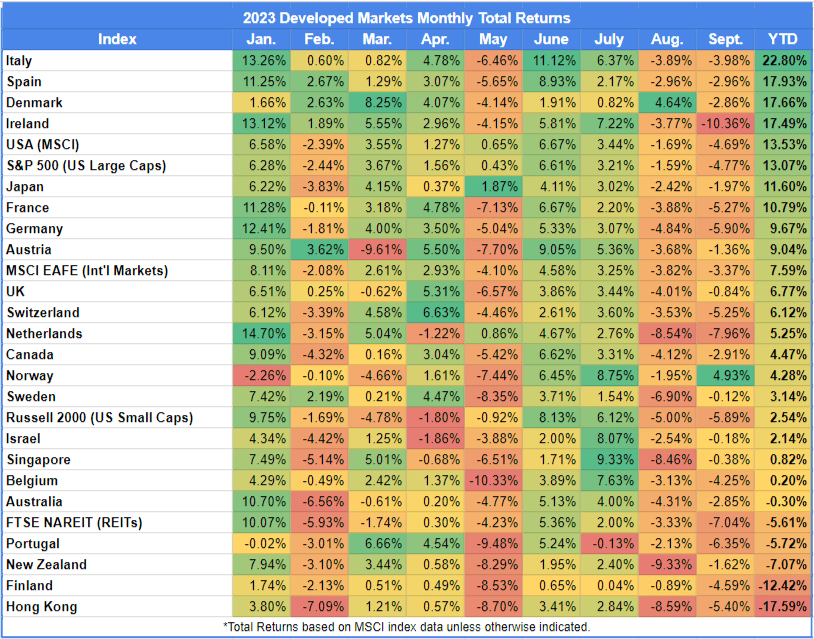

There are four tables below. The sector, developed market, and emerging market tables break down 2023 returns by month. The global returns table shows 2023 returns by quarter.

Nine months into the year, the tables offer a few broader lessons for investors:

- Markets and media provide a constant stream of excitement and worry for every investor. Enough use it as an excuse to act, that it moves market prices too far in one direction. Except, what seemed worrisome or exciting often turns out to be ho-hum, creating the conditions for markets to overcorrect in the opposite direction. That bias towards action comes at a cost that often leaves investors worse off than had they done nothing.

- You earn long-run returns by surviving the short term. You can try to predict the swings (good luck) or you can embrace a bumpier ride. The monthly and quarterly swings remind us that returns earned over time don’t come easy.

- Diversification means always holding something uncomfortable in your portfolio. The tables below are a good example of how losses in one market are made up for by gains in another. And yet, a diverse portfolio eliminates the guesswork of finding where the best returns come from in any given year.

Some lighter observations on the recent quarter:

- The majority of developed and emerging markets saw losses in the third quarter of 2023. Only four developed markets rose in Q3. Only nine emerging markets rose in Q3 — four of the nine rose less than 1% in the third quarter.

- With two exceptions (Egypt and Turkey), every developed and emerging market experienced a selloff in August and/or September. All but two developed markets (Denmark and Norway) sold off in both months. 16 of the 24 emerging markets sold off in both months.

- The three worst-performing sectors last year — Communication Services (-40%), Info Tech (-28%), and Consumer Discretionary (-37%) — are the best-performing sectors through three quarters this year. Of the three, only Communication Services saw a gain in the third quarter.

- The Energy sector was the only sector with a positive gain in each month of the third quarter, up 12% in Q3, and 6% year to date.

- The Utilities sector is the only sector with losses over the last three consecutive quarters. It’s down 14% year to date.

- If I told you Turkey lost 19% through Q2, what do think its return would be on the year? It experienced a 9% loss through Q1. That worsened to a 19% loss through Q2. Then it had a remarkable 19% gain in July, an 8% gain in August, and a 3% gain in September. That’s a 32.8% gain in Q3 alone and gives Turkey a 7.8% return year to date. Markets can turn quickly and when you least expect it.

- Turkey’s 19.3% return in July is the best single-month return for any emerging or developed market this year. However, its 32.8% return in Q3 falls just shy of the best quarterly return in 2023 by the Czech Republic at 33.0%.

Related Reading:

2023: Q1 Returns

2023: First-Half Returns