To say big tech is driving US markets this year would be an understatement. Through two quarters of 2024, the S&P 500 gained 15.3%, with dividends. Only two U.S. sectors performed better than that, as you’ll see below.

Much of the market concerns lately center around the AI boom and market concentration. Some of it is warranted but market concentration is nothing new and not all booms turn into wildly speculative bubbles. That hasn’t stopped folks from comparing the current boom with past bubbles to add weight to their predictions.

For tech innovation, it’s natural to look at the last time a new technology took the stock market by storm. The Dotcom Bubble is the most convenient choice. It’s the most recent, a good chunk of today’s investors lived through it, and the tech behind it was transformational.

Unfortunately, the AI boom is nothing like the Dotcom Bubble. At least, not yet.

Yes, there are similarities. New emerging technology, talk of a “New Era” that will transform life and work, high and rising valuations, unexpected companies hitting record-high market caps, old-world companies slapping “AI” on products to get in on the hype (much like they did with “.com”), and so on.

But the differences are stark. The AI boom is concentrated in a handful of companies. The Dotcom era was the opposite. The Dotcom Bubble saw a mad rush of IPOs, sky-high demand for shares, hundreds of companies going public that you would barely call companies with little to no sales, nonexistent earnings, and made-up metrics to make up for the lack of sales and earnings.

Maybe the current AI boom will hit that level of insanity in the future. The speculation rampant at the peak of the Dotcom Bubble took time to grow to a level of euphoria not seen since 1929. Maybe it’s still early days for AI. Maybe massive investment in hardware and infrastructure is needed — like the early days of the internet — to make AI the “next big thing,” which could take a few years to build out.

Or maybe AI is not all it’s hyped up to be. Maybe it’s more BS pattern recognition than intelligence. The downside of any innovation is that we never know for sure how much is hype versus fantasy until after the fact. That’s the risk of investing.

What we know today is that the market, at least, believes some of the hype. Performance in the S&P’s Tech and Communications sectors outpaced the S&P 500 by almost double so far this year. Every other sector has underperformed. That outperformance has led to concerns about market concentration in the top 7 companies that make up over 30% of the S&P 500.

The good news is that if you own an S&P 500 index fund or similar large-cap fund, you benefitted from the performance of those companies this year. The downside is that the benefit of diversification that comes with most index funds is now a potential liability. A handful of stocks now make up a larger portion of your portfolio. How much larger depends on how broadly diversified your portfolio is. So what should an investor do?

- Don’t overreact. Six months is a tiny window in an investment time frame of 10 or more years. It tells us nothing about how the next decade or more will play out. Drastic changes to your portfolio in the short term often lead to long-term mistakes.

- A sound investor with a diversified portfolio owns more than a single large-cap index fund. So that 30% concentration in 7 stocks is not 30% of the overall portfolio. It’s watered down by international funds, small-cap funds, bond funds, and so forth. It’s a much smaller percentage of the total portfolio.

- Much of investing is about finding a balance between comfort and risk-taking to earn a return. If your allocation in large-cap stocks makes you uncomfortable, adjust it lower and diversify outside that asset class, to where you’re comfortable again.

- If you’re diving into the AI hype expecting to make a lot of money quickly, you also must accept that you could lose money just as fast. The possibility of losing is easy to overlook because everyone expects to make money when they buy a stock. That’s not always the case. Stocks that rise in price very fast over short periods, can fall in price equally fast.

- If the AI hype is overblown/overextended, then the biggest risk is concentrated in a handful of the largest stocks. That’s not to say there won’t be collateral damage if it leads to a market panic. Just that the primary damage should be concentrated in those stocks.

- Market concentration is nothing new. It swings between greater and lesser concentration throughout market history. The current high concentration will likely correct itself as it has in the past…eventually. And a list of the 10 biggest companies a decade from now will look different from that list today.

A note before getting to the first-half highlights. The asset class, sector, international markets, and emerging market return quilts are up-to-date with the Q2 returns. Hit the links for each one.

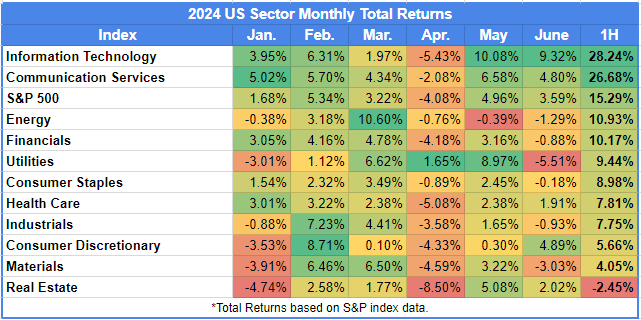

There are four tables below. The first is a monthly breakdown of U.S. sector performance for 2024, followed by tables for developed and emerging markets. The last table is a quarterly breakdown of global market performance.

Here are a few highlights:

- Big tech is the story around markets. The S&P 500 performed great so far but that’s about it. Small caps have not. Mid caps have not either. Broad international and emerging markets fell short of the S&P. And within the S&P 500, there is an obvious deviation between Tech and Communication stocks and everything else.

- The Tech sector gained 28.2% in the first half of the year. Performing slightly better in the second quarter than it did in the first. The Communication sector came in at 26.7% through the second quarter. Both were more than double that of the next best sector.

- Every other U.S. sector underperformed the S&P 500. Energy was the third best at 10.9%. Then Financials at 10.2%. It dwindled lower from there. As mentioned, the story is AI and big tech. We’ll see how long it lasts.

- Real estate was the only U.S. sector that lost money year to date at -2.5%. It saw losses in both quarters this year.

- To continue on that sour note, 5 countries — all emerging markets — also experienced losses in both quarters of 2024 — Qatar, Chile, Thailand, Brazil, and Egypt.

- On the bright side, only four developed markets lost money year to date. So 17 developed markets, including the U.S., were higher, with Denmark, Netherlands, and Ireland outperforming the S&P 500.

- Despite, 10 out of 24 emerging market countries losing ground, the broad emerging market index gained 7.7%, including dividends.

- Only one country experienced gains in every month this year — India. It’s rare. As you can see from the tables, most markets have pullbacks and advances during bull and bear markets.

- Six countries turned a first-quarter loss into a year-to-date gain thanks to an improved second quarter — South Africa, China, Switzerland, Czech Republic, Norway, and Finland.

Related Reading:

2024: Q1 Returns

2023: A Year in Returns