A lot can happen in a few short months in markets. The U.S. market went from a crash to a recovery to new highs in five months.

It began with the announcement of tariff rates not seen since the 1930s. Then they were delayed. A similar pattern has followed since. Threaten tariffs, announce tariffs, delay announced tariffs, delay some more, and repeat.

The market, at this point, seems to be pricing in the existing tariffs with further delays on anything higher. The risk is that the pattern changes.

The other notable issue this year is the declining dollar. Currency risk can enhance or negate returns depending on where and how your money is invested.

For example, the dollar relative to the euro is down about 11% through the first half of the year. The falling dollar explains a portion of the performance of foreign markets this year. Countries in the MSCI EAFE and EM index, that use the euro, are all up more than 11% year to date.

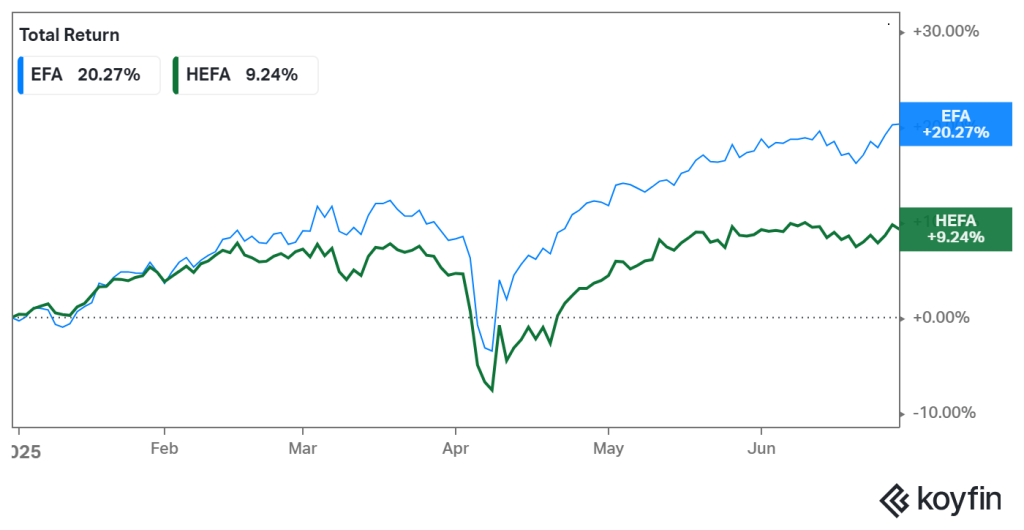

Another way to look at it is the chart below. It shows the dollar-hedged (HEFA) versus unhedged (EFA) MSCI EAFE ETFs. Most investors own unhedged funds, for good reason. It offers currency diversification and avoids needing to predict big currency exchange shifts because it’s difficult to do.

The unhedged (EFA) ETF is up almost exactly 11 percentage points more than the hedged (HEFA) ETF. Currency risk can be a benefit with a diversified portfolio in the short run (European investors, with money in U.S. stocks are experiencing the opposite effect). In the long run, currency risk tends to balance out.

A quick note before we get to the highlights. The asset class, sector, international, and emerging market returns are up to date through June 30, 2025. Hit the links for each.

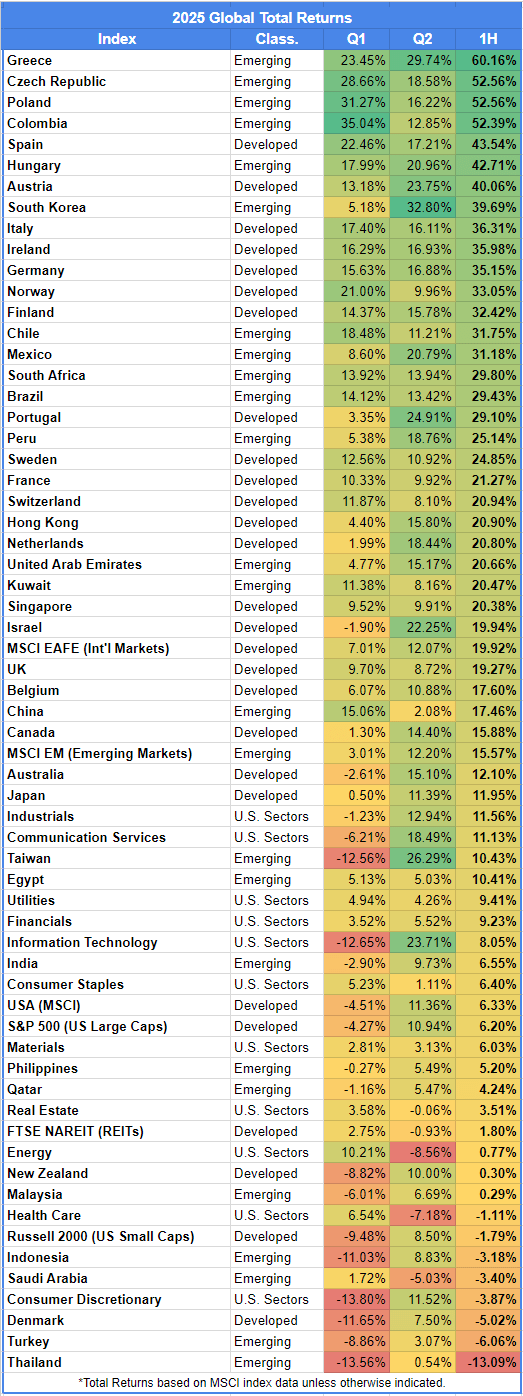

You’ll find four tables below: U.S. sector, developed markets, and emerging markets performance by month, with the last table showing quarterly returns of all three combined.

Here are a few notable highlights:

- The three worst performing U.S. sectors in Q1 (Comm Services, Info Tech, and Consumer Discretionary) were the best performers in Q2. Only two of the three are positive year to date. Consumer Discretionary is the worst performing sector despite its rebound in Q2.

- The two best performing sectors in Q1 (Energy and Health Care) were the worst performers in Q2. Both are close to even on the year.

- In another case of markets are hard to predict, I doubt anyone expected the industrial sector to be leading halfway through 2025.

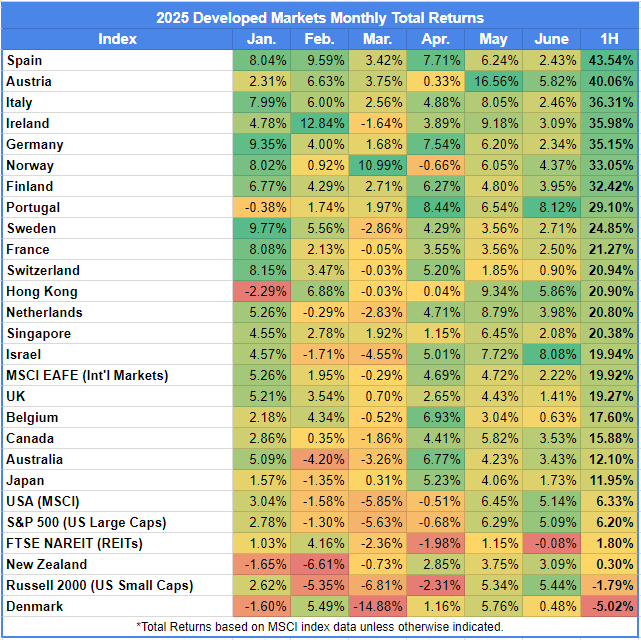

- Denmark is the sole developed country in the red, with a 5% loss to date. The largest holding in its index, with a 22% weighting, is down around 27%. It’s a perfect example of concentration risk that might exist in some single country funds. (Denmark is not on the Euro. Its Krone has seen a similar currency shift relative to the dollar as the Euro, though.)

- Over half of the developed markets in the MSCI EAFE are up 20% or more through June, with a third up 30% or more. The top two, Spain and Austria, exceed 40% (Austria, just barely).

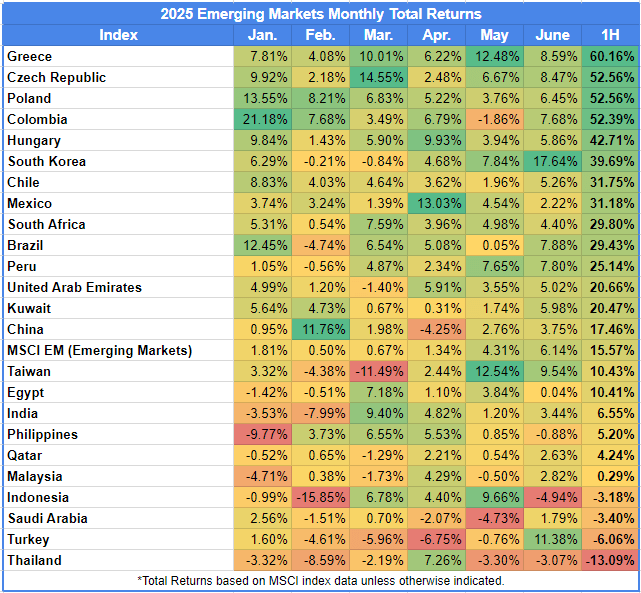

- Emerging markets show a similar trend. Over half of the emerging markets are up 20% to date, with a third up 30% or more. The top four exceed 50% through June.

- Greece was the lone market with returns in excess of 20% in both Q1 and Q2 2025.

- The performance of international markets, this year, is a perfect example of why diversifying a portion of your portfolio outside the U.S. is prudent.

Related Reading: