For the past four years investors have been on a quest for higher yield as the Fed has pushed rates lower to spur economic growth. It’s been a double-edged sword. With savers being gouged by lower rates, investors have thrown risk out the window in search of higher yield. Since 2007, over $1 trillion has poured into bond funds.

For the past four years investors have been on a quest for higher yield as the Fed has pushed rates lower to spur economic growth. It’s been a double-edged sword. With savers being gouged by lower rates, investors have thrown risk out the window in search of higher yield. Since 2007, over $1 trillion has poured into bond funds.

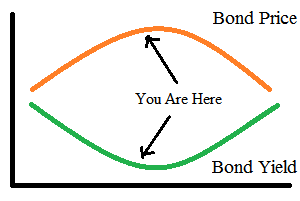

That’s a healthy sum of money. And investors have been rewarded, thanks to Fed policy. But how long will it last? Is now the best time to continue that trend? At some point interest rates will rise. Maybe next month. Or next year. The 30 year bull market in bonds will eventually end. And savers will rejoice in higher interest rates. That’s if their bond over allocation doesn’t hurt them in the process.

Until then, should investors really keep putting good money into an overpriced asset? When bond prices and yields move in opposite directions, common sense would tell us no.

The Bond Market Flood

Nothing has fueled bonds more than fear in the stock market. Since the financial crisis, more money has poured into bond funds than equity funds. Call it the great equity exodus. The stock market crashed and investors looked for safety. Bonds were earning a nice yield at the time. The 10 year Treasury was almost 4%. So the money flowed in and investors were happy.

Then the Fed intervened.

Since 2007, interest rates have slid to all time lows. In turn, bond funds have outperformed along the way. This only fueled more investment in bonds since nothing is more convincing than past performance.

And the trend doesn’t seem to be slowing either. As much as savers need higher interest rates, current bond fund owners may not like the outcome.

The First Domino To Fall

The latest search for yield has driven investors into high yield bonds. Some have thrown bond ratings out the window taking their chances on junk bonds. In turn, demand has pushed these bond prices higher.

Call it a slow motion car wreck or high-speed collision. It just depends on how quickly rates move. But high yield bonds will be the first casualty. The default risk alone never warranted these bonds as a safe investment. Once rates rise, investors will find competitive, safer yields and move their money.

Shorter over Longer Term

If you’re invested for the long-term the theory is simple, allocate less into bonds. If you can’t do that, then allocate into short-term bonds over long-term bonds. This should limit your losses.

Any increase in rates will push bond prices lower. Eventually it will make long-term bonds more attractive to own. Until then, you can lower your interest rate risk by focusing on the short-term.

Bonds Over Bond Funds

Most investors use bond funds over individual bonds for the diversification. But it comes with one big drawback. Bond funds, unlike bonds, never have a maturity date. The underlying bonds in a fund do, but whether they are held that long will depend on the fund manager.

With a bond, the value may increase or decrease over time, but eventually you get the principal back in full. This isn’t true with bond funds, where fund managers continually buy and sell holdings to boost performance (or limit losses). Be aware of your fund managers ability or drop them altogether for a short-term bond ETF.

What About Inflation?

Then there are TIPS? The saviors of your purchasing power. TIPS (Treasury Inflation Protection Securities) offer investors a hedge for inflation.

The inflation fear has been overhyped so far. The belief has been that inflation will soon run rampant. This fear has been ongoing for the past four years, even though we have yet to see it happen.

Let’s play devils advocate for a second. What if the inflation risk is overdone. Now TIPS owners overpaid for the opportunity to protect themselves from something that won’t happen. TIPS are currently paying a negative real rate of return. So TIPS haven’t been the answer either.

Besides if interest rates rise before inflation does, you still miss out on higher rates. And it would push TIPS prices lower.

Common Sense Strategy

You need to remember one simple rule. Buy low, sell high. Common sense tells us when something is overpriced, we should sell it. And reducing your risk over time is a simple strategy to undertake. Especially when it’s staring you in the face.

At some point the price of bonds will normalize as interest rates rise. They may even become undervalued if too many investors freak out from the falling prices. If that happens you should buy. Until then, play it safe. Reduce your risk. Take some profits. And wait for prices to fall.