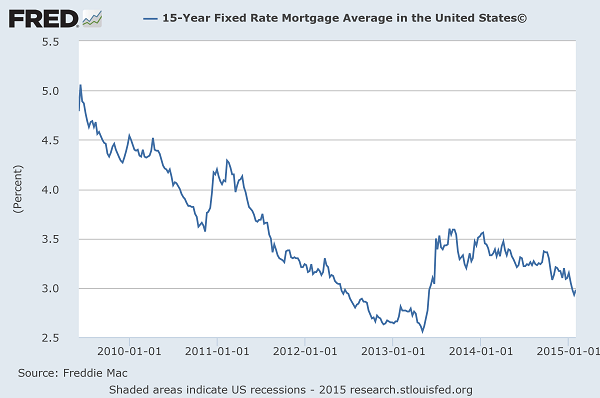

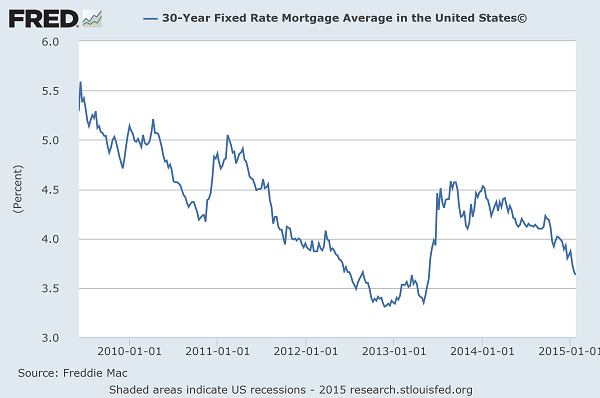

I don’t know anyone who thought interest rates would stay low for this long or go lower. But falling rates do have one benefit. All you homeowners out there have another opportunity to refinance your mortgage. Mortgage rates fell for most of 2014 to rates we haven’t seen in two years.

Two years ago it looked like the last great chance to lock in historically low mortgage rates. If you missed it, the market gave you a second chance. Current 15 year and 30 year mortgage rates are getting close to those all time lows. You can check the FRED charts below.

It’s gotten really easy to shop for a mortgage. I mention a few places to start in the financial tools page. It might be worth checking your local bank or broker too. The advantage to refinancing is simple. Your mortgage is probably your biggest monthly expense. Refinancing to a lower rate, lowers that expense and gives you options.

One option is to funnel that freed up money back into the mortgage to pay down the principle. This pays off your mortgage faster, lowers your total interest costs, and you’ll fully own your home sooner. Another is to put it toward paying down higher rate debt. Or you can put it toward savings. In all three cases it’s less money for the bank and a win for you.

Before you rush out to refinance, there are a few things you need to consider, like fees, costs, penalties, and more. The Federal Reserve has a handy guide covering it all. I suggest reading through it first.

Last Call

- Dividend Stocks: How to Invest When Valuations Are Expensive – AAAMP Blog

- A Dozen Things I’ve Learned from Joel Greenblatt about Value Investing – 25iq

- 12 Thoughts About Investing and the Economy – M. Housel

- Recency Bias Damages Returns – L. Swedroe

- “The Search for Yield” Trilogy – Vanguard Blog

- Why Passive Investing Makes Even More Sense in Inefficient Markets – Morningstar

- The Small-Firm Effect Is Real, and It’s Spectacular – AQR