The broad lesson from this year’s Berkshire annual meeting is that successful investing is hard. Especially when it appears to be easy.

Of course, that will likely be the lesson when we look back on this period a decade from now too. But until then, Warren Buffett and Charlie Munger will again be labeled “old and out of touch” with the new reality.

Before diving in with the lessons, here’s a quick tip: if you want to listen to the entire meeting, bump the speed up to 1.2x or higher. It goes by faster and Buffett and Munger sound 30 years younger.

Let’s dive in.

It’s hard for companies to stay on top.

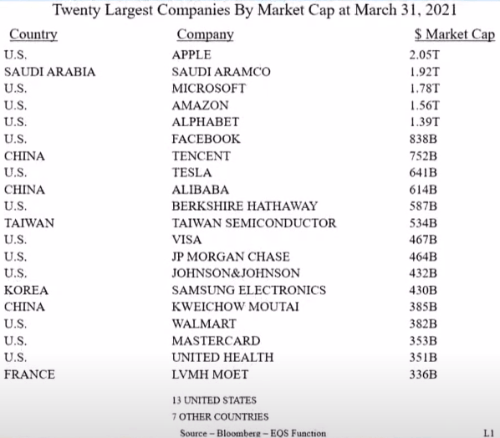

Buffett showed a list of the 20 largest companies, by market cap, in the world today.

He then asked, “how many of those companies are going to be on the list 30 years from now?”

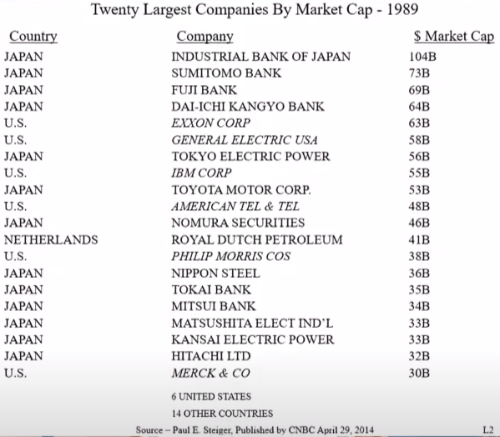

To bring his point home, he pulled up a list of the top 20 from 1989.

If you look at the top 20 from 1989, there’s two things that should grab your interest. At least two. None of the 20 from 30 years ago, are on the present list. None. Zero. There were then six US companies on the list and their names are familiar to you. We have General Electric, we have Exxon, we have IBM Corp… And I would guess that very few of you, when I asked you to play the quiz a little, a few minutes ago, would’ve put down zero… It’s a reminder of what extraordinary things can happen.

And if you look at the top company at that time had a market value of a hundred billion, 104 billion. So the largest company in the world, in just a shade over 30 years has gone from a hundred billion to 2 trillion. And at the bottom, the number 20 has gone from 34 billion to something little over 10 times that… But it tells you that capitalism has worked incredibly well, especially for the capitalists. And it’s a pretty astounding number. You’d think it could be repeated that 30 years from now that you could take 2 trillion for Apple and multiply any company and come up with 30 times after the leader. Yeah, it seems impossible and maybe it is impossible, but we were just as sure of ourselves as investors and Wall Street was in 1989 as we are today, but the world can change in very, very dramatic ways.

The strength and greatness of the current top 20 companies is obvious. But if history is any guide, some will falter, growth will slow for others, and/or the market will de-value them over the next 30 years. And each one will be replaced in the process. There’s a good chance that companies that don’t exist today will be on the list three decades from now.

In fact, a similar list would show significant changes from decade to decade. As Buffett states: “the world can change in very, very dramatic ways.” There are numerous reasons why. First, it’s difficult for big companies to continue to grow at the high level that made them so big. Second, innovation and creative destruction are features of the system. Third, valuation at any point in time is a combination of a company’s future growth and market sentiment. Even if a company can continue to grow at a high rate, the market may not agree.

The hard reality is the average business has a short lifespan. That’s why investing is so hard. Correctly picking who falls and who rises in their place is difficult. It’s just as difficult to hold onto a company that falls because sentiment wrongly thinks its time has passed.

It also shows how difficult it is to make concentrated long-term bets and succeed. Buffett said it’s an argument in favor of a more diversified approach (he mentions index funds). Owning a bigger basket of stocks improves your chances of owning the few that rise to the top every decade.

Most companies in new industries fail.

I thought I’d put up the list of auto companies from over the years. And I was originally going to put up just the ones that were the M’s, so I could get them on one slide. But when I went to the M’s, it went on and on and on. So I just decided to put up the ones that started with “Ma,” and as you can see, there were almost 40 companies that went into the auto business, just starting with MA…

There were at least 2,000 companies that entered the auto business because it clearly had this incredible future. And of course you remember in 2009, there were three left, two of which went bankrupt. So there’s a lot more to picking stocks than figuring out what’s going to be a wonderful industry in the future. The Maytag company put out a car. Allstate put out a car. DuPont put out a car. I mean, Nebraska, there was Nebraska Motor company. Everybody started car companies just like everybody’s starting something now… But there were very, very, very few people that picked the winner… So I just want to tell you, it’s not as easy as it sounds.

There are numerous examples of this over the last century. It happened with televisions. The computer industry saw it. The hard drive industry had over 70 competitors at its peak (and offered several lessons from it). Each one led to excesses in investment and valuations before it blew up.

Again, it might be easy to see the immense potential for a new industry, but it’s hard to know which companies come out on top. In fact, the best time to invest in a new industry might be after it implodes because only a few surviving companies remain to compete for market share.

The latest speculation.

Imagine being able to own parts of the biggest businesses in the world and putting billions of dollars in them and take it out two days later. I mean, compared to farms or apartment houses or office buildings, where it takes months to close a deal, the markets offer a chance to participate in earning assets on a basis that’s very, very low cost and instantaneous… But it makes its real money if they can get the gamblers to come in because they provide more action and they’re willing to pay silly fees and all kinds of things. So you have this incredible, a huge asset to humanity, but it really makes its money when people are doing stupid things. I mean, that’s where the money really is.

And Keynes wrote this in 1936…in The General Theory, that “Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital of element of a country becomes a by-product of the activities of a casino, the job is likely to be ill done.”

We’ve had a lot of people in the casino in the last year. You have millions and millions of people who’ve set up accounts where they day trade. Where they’re selling puts and calls… I would say that you had the greatest increase in the number of gamblers essentially… And they actually don’t have a lot of good results. And if they just bought stocks, they’d do fine and held them.

But the gambling impulse is very strong in people worldwide, and occasionally it gets an enormous shove and conditions lead to this place where more people are entering the casino than are leaving every day. And that creates its own reality for a while. And nobody tells you when the clock is going to strike 12:00, and it all turns to pumpkins and mice… This is about as extreme as we’ve seen it.

The market goes through periods of speculative excess where the draw to get rich quickly overwhelms everyone. The sad part is people actually try to get rich trying to replicate Buffett’s very first line in the quote above. They buy a portion of a business in the stock market and two days later they sell it. Or instead of a stock, they buy the option to buy or sell a stock, only to sell it two days later.

In either case, a few get lucky doing this. They make a decade’s worth of returns in a few months. Their “success” is splashed over the headlines and it draws more people in. Simply put, it’s hard to watch other people make money and not want to join in. This is true even if you recognize the speculation going on.

However, the overwhelming outcome of every speculative period is losses. Even those who make money early on, ultimately lose, because they can’t stop. They try to grab every last penny only to realize too late that they missed the top.

It’s because speculative episodes don’t end in a glorious crash. Instead, speculators are faced with a series of dips. But unlike prior dips that rebound to new highs, this rebound falls short and is followed by another dip lower than the last…then another dip lower…and another…and then it crashes. So the top, that everyone thinks they can time, only looks obvious in hindsight.

The biggest risk factor.

The number one risk factor is that this business gets the wrong management, and you get a guy or a woman in charge of it that they’re personable, the directors like them, they don’t know what they’re doing, but they know how to put on an appearance. That’s the biggest single danger that a business has, and that that person stays and runs it for 10 or 15 years… I’ve looked at a lot of businesses and that’s what’s caused the number one problem.

As if picking winners isn’t hard enough, companies are one bad CEO hire away from destroying shareholder value. The fact that the destruction happens gradually, instead of immediately, makes it worse. It also means that true long-term investors need an extra skillset to see through the BS and accurately judge someone’s character and ability.

The Dream business.

We’ve always known that the dream business is the one that takes very little capital and grows a lot. And Apple and Google and Microsoft and Facebook are terrific examples of that. I mean, Apple has $37 billion in property, plant, equipment. Berkshire has 170 billion or something like that. They’re going to make a lot more money than we do… We found that out with See’s Candy in 1972. I mean, See’s Candy just doesn’t require that much capital. It has, obviously, a couple of manufacturing plants. They call them kitchens. But it doesn’t have big inventories, except seasonally for a short period. It doesn’t have a lot of receivables…

They’re the best businesses, but they command the best prices, too. And there aren’t that many of them and they don’t always stay that way. We’re looking for them all the time… That’s what capitalism is about. People getting a return on capital. The way you get it is having something that doesn’t take too much capital.

Every company requires a certain amount of money to be spent to produce the profits it makes each year. The best companies require a small amount of money each year to produce a lot of profits. They also have some advantage — Buffett’s moats — protecting their ability to produce huge profits.

The problem for investors is those dream companies trade at a premium in the stock market — the better the company the higher the premium. And paying too high of a premium for most companies is a recipe for disaster.

And they’re not nearly as prevalent or easy to identify as everyone thinks. Because every stock trading at a premium has a story about how great the company’s future will be but that doesn’t make it a dream business. Management still has to execute, build a moat, and fend off competition for years before it becomes obvious to most people that it’s great.

But the investors who really make money identify these dream businesses way before everyone else. It’s one more thing to add to the long list of reasons why investing is so hard.

Sources:

Berkshire Hathaway Annual Meeting 2021

Transcript: Berkshire Hathaway Annual Meeting 2021

Last Call

- Lessons from The Chocolate Wars – Fortune Financial

- The Limits of Investing Sanity – M. Housel

- Why Do Fund Investors Neglect Base Rates? – Behavioural Investment

- U.K. Value Factor: The 200+ Year View – Two Centuries Investments

- Corporate Taxes Don’t Matter – Klement on Investing

- The Architecture of Tomorrow: An Interview With Ben Horowitz – Time Well Spent

- Crazy New Ideas – P. Graham

- Efficiency is the Enemy – Farnam Street

- Why It’s Nearly Impossible to Buy an Original Bob Ross Painting – The Hustle