Electricity was a fledging industry in the 1890s. Samuel Insull was at the center of its transformation and growth.

Samuel Insull got his start as a stenographer in London. After losing his job, he found an opening at Thomas Edison’s new telephone company, applied, and was hired as the bookkeeper and secretary for the London manager.

As fate would have it, a job opening in America changed everything. Edison needed a personal secretary. Insull made his interest known. At age 21 (1881), he was off to the U.S. to work alongside the great inventor. Edison recognized Insull’s potential and he quickly moved up the ranks.

Within 11 years, he was offered a vice-president position in Edison’s General Electric Company. Insull, unhappy with the offer (he expected a higher position), took charge of Chicago Edison Company instead in 1892.

Insull believed that mass production and scale was the future of the electric utility industry. The efficiencies that came with size lowered costs, lowered rates for customers, and boosted profits for shareholders. It was a win-win all around. But that meant Insull needed to monopolize Chicago’s electric grid.

By 1895, he acquired enough of the city’s 30 existing electric companies to control everything within Chicago Edison’s given territory. Two years later he formed Commonwealth Electric Light & Power Co. to sweep up most of the rest. Insull merged the two companies in 1907 to form Commonwealth Edison Company (ComEd). Commonwealth Edison bought the Cosmopolitan Electric Co. six years later to make it the only electric provider to Chicago. Commonwealth Edison became Insull’s first holding company. It was not his last.

The concept of a holding company emerged at the tail end of the 1800s. It was used to consolidate control of two or more companies under one management. The benefit was more efficient management and economies of scale in a growing industry. In a high growth industry, like electric utilities, a holding company made it easier to secure favorable financing terms, could plan and build networks for entire regions of the country, and could hire top engineering talent to work across multiple operating companies. But like any new financial innovation downsides emerge when taken to extreme.

After locking up control of Chicago’s utilities, Insull looked outward. He formed the Middle West Utilities Company in 1912 to acquire more utilities. He designed it in such a way that his tiny initial investment gave him complete control despite issuing shares to the public. In fact, Insull made his initial investment back (and then some) thanks to the eagerness of new investors. He sold the entirety of his preferred shares and 10,000 of his 60,000 common stock for more than he put in.

Over the next five years, Insull by way of Middle West Utilities, bought up utilities across 13 states. However, the outbreak of WWI gave Insull a game-changing idea that helped expand his empire further.

Liberty Bonds funded the war effort. Insull led Illinois’s State Council of Defense. Its purpose was a public relations machine. The goal was to shift the public perspective, induce patriotism, and sell Liberty Bonds.

Insull learned firsthand what the power of public relations, advertising, and an aggressive salesforce could accomplish. He promoted the wonders of electricity and improved the public’s view toward his electric utilities. He signed up new customers at a faster rate. Most important, he sold common stock and, more so, preferred stock and bonds to the public to fund his growth. Specifically, he targeted his own customers and employees.

The promotional efforts had a massive impact on Commonwealth Edison and Middle West Utilities. From 1919 to 1921, the number of stock and bondholders in Illinois alone rose from 50,000 to almost 500,000. Electricity use more than doubled from 1915 to 1925 in Chicago. Middle West now served customers in 32 states. But Insull’s success brought competition.

The 1920s created the perfect environment for the expanded use of holding companies. A burgeoning new industry combined with an extended bull market full of investors eager to buy shares led to a race to consolidate at all costs. Demand for securities was so high that stock and bond promotion became the more lucrative business.

The big money was made in selling stock to the public for more than you had had to pay for it (or, to put it another way, in selling the stock of your own company to yourself for less than its potential market value.) To do this, you had of course to put a high—if not actually extravagant—valuation upon the property which the stock represented, and to paint a rosy picture of possible earnings. And to make good on this picture, you had to provide the earnings. Ordinarily, the operation was one which could not soon be repeated without disastrous results: even in a rapidly growing industry, it usually took time for earnings to catch up with expectations. But possibly ways of finding them—or seeming to find them—could be discovered.

Pyramiding became the strategy du jour. New holding companies formed at an accelerated rate. One piled on top of another. Each one issuing stocks and bonds to raise money to buy more electric and gas companies, holdings companies, or both. Each one syphoning profits from its collection of companies to pay dividends to common stock shareholders and pass any excess profits up the chain to the next holding company.

Ordinarily the holding company held only the common stock of the operating companies, or part of it, leaving the bonds and preferred stock in the hands of the general public. If we think of the earnings which went to pay interest on the bonds and dividends on the preferred stock as resembling the milk in a bottle, and the further earnings which went to pay dividends on the common stock as the cream at the top, we can see how advantageous it was to skim the cream from ten or twenty bottles: one inch more of cream in each bottle, and the cream-separators would find their haul growing out of all proportion. (Conversely, of course, the cream-separating business would languish if the cows gave a poorer quality of milk—but that is the sort of thing which does not occur to investors in boom times.)

By piling holding companies on top of one another, one could still further increase the richness of one’s cream… To own the common stock of a super-holding company might be to get the best of the extra-heavy cream, skimmed, as it were, from forty or fifty bottles (again, if there was any).

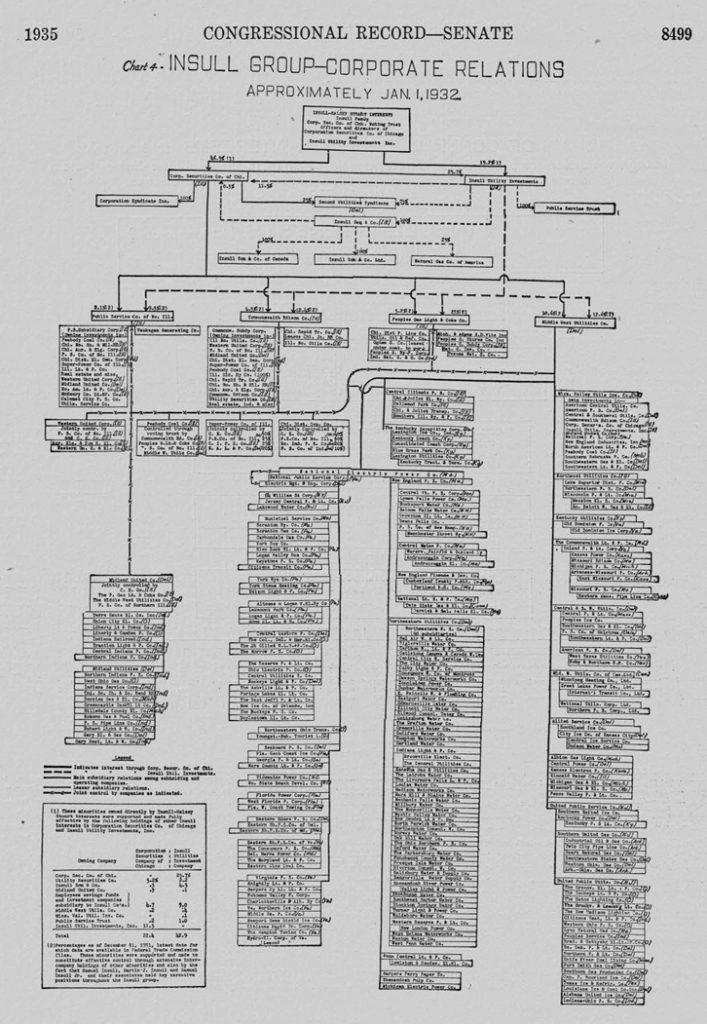

By 1929, Insull sat atop a pyramid of holding companies upon holding companies multiple levels deep. It controlled an array of electric companies, gas companies, coal mines, paper mills, textile mills, a shoe factory, a tire factory, and several real estate companies. At the height of his buying spree, he paid upwards of two to three times the worth of a company. It only fueled the rise in utility company stock prices.

At the top of the pyramid was Insull Utility Investments, Inc. It held stock in four holding companies: Commonwealth Edison, Middle West Utilities, Public Service Company of Nothern Illinois, and Peoples Gas Light and Coke. Below that was a complex web of operating companies within holding companies within holding companies.

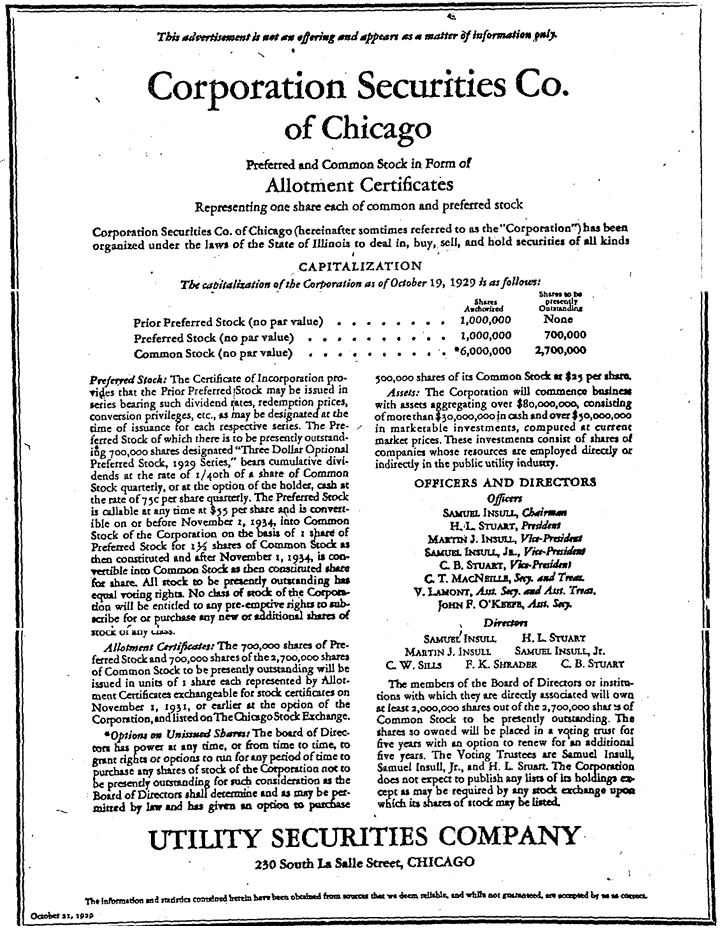

Amid this confusion and complexity was one notable problem. Insull fell short of complete control of the pyramid. He needed one last deal. To solve this problem, and ensure control, Insull formed one last holding company to control everything.

In October 1929, the Corporation Securities Company of Chicago was formed. Within days, ads like the one below dated Oct. 21, 1929, promoted the new offering in the Chicago Tribune.

Insull’s solution worked…until the Great Crash hit on October 28 and 29. The effect wasn’t immediate. Rather, it led to a slow-motion collapse that forced Insull to do everything to keep numerous stocks aloft. He offered public reassurances summed up by “business as usual” along with capital expansion pledges, guarantees against margin calls for his employees, stock pools to manipulate prices, new bond offerings to raise funds to cover existing interest payments and growth pledges, payment of dividends in shares instead of cash, and company holdings as collateral for more debt. It only postponed the inevitable. Finally, as a last-ditch effort, Insull put up all of his own stock as collateral to keep his company afloat.

On April 8, 1932, the weight of all its debt came due. The pyramid collapsed. Insull lost his shares and control of his empire.

In all, by January 31, 1932, the Insulls had formed more than ninety-five holding companies and two hundred and fifty-five operating companies. The investment which the Insulls had made to secure the direction of this pyramid was something less than one million dollars. If we consider the market value of their holdings in March, 1930, it amounted to more than $100,000,000. This $100,000,000, in turn, now controlled $2,500,000,000. For every dollar that the Insulls originally invested, they now controlled $2,500 of the public’s money.

Yet, the entirety of its worth was an illusion. Arthur Anderson & Co., appointed auditor, found Insull’s pyramid built on fraud. Notably, assets were sold back and forth between companies to inflate their value and profits and game the books. The complexity helped hide the underlying fraud.

Insull became the scapegoat for much of the financial and regulatory reformers that followed. He faced criminal charges in Chicago, played fugitive after fleeing the country, extradited from Turkey in 1934, but acquitted of all charges. He died four years later in Paris of a heart attack with an estate of about $1,000.

Insull wasn’t the first, nor the last to turn to fraud to keep his empire growing. He put all his hopes in the idea that electricity demand would never see a significant slump. He was right. Revenue held up well for the industry throughout the Great Depression.

Instead, Insull put his faith in the wrong thing. The structure he created was built on a massive amount debt and needed an endless demand for security sales (amid rising prices) to keep his empire from falling. He took advantage of the 1920s bull market only to learn that what he thought was impossible, was inevitable.

The unsurprising lesson is how often financial folly reveals itself after a market bust.

Sources:

Related Reading: