What appeared to be a great start to the year has since cooled off. The S&P 500 has had a great year in only eight months. Bonds became a real downer in a very short time. Europe is showing signs of life. Emerging markets have done so poorly, for so long, it might be the next big opportunity. The Fed has done nothing since it announced a planned future possibility of tapering. And the market impatiently throws temper tantrums in the hopes of finding out.

Caught amid all that, investors are scrambling to make up the difference. In the end it still comes down to proper allocation. As is always the case, the question becomes where do we go from here?

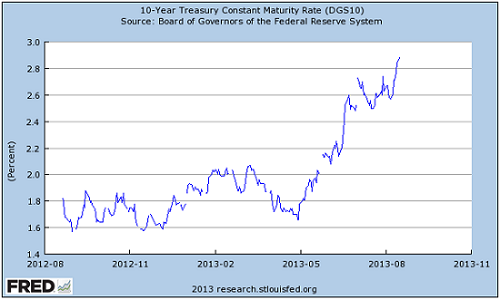

Bonds

What do you get when something goes from 1.6 to 2.9 in 3 months? A 10% loss in 10 yr Treasury bond prices. It’s the largest percentage increase 10 yr Treasury rates ever. Seriously. That’s the bad news.

Here’s more. That increase affected REITs, utility stocks, bonds and bond funds of all duration, and every dividend paying stock. So basically everything. And interest rates are still considered low. At least below normal. And we’re moving towards normalized rates.

Normalized, of course, is closer to where things were before QE began. That would put the 10 yr Treasury around 3% to 3.5%. If I were a betting man, I’d put my money on a move higher. Uncertainty around Fed tapering leaves the bond market and interest rates deciding the fate of everything.

One thing is certain, we’ll be seeing a new Fed Chairman (or Chairwoman) in a few short months. Despite what many believe to be a September start to tapering, that appointment will largely decide the fate of Fed tapering going forward, the direction of interest rates, and give much-needed certainty to the markets.

S&P 500

Since the 2009 lows, the S&P 500 is up 141%. That’s a great run for any time period, much less one where the sky was always falling at every turn. You could easily have said that last year and made changes thinking it couldn’t go higher. I’m sure many did.

There are two ways to play this going forward: rebalance your portfolio or underweight the better performing allocation. Rebalancing is something you should be doing regularly.

The idea is very simple. When you have one area of your portfolio do very well for so long, you move some of that money into the worst performing areas to return you to a predefined allocation. This allows you to take advantage of the poorer performing, undervalued markets and let mean reversion take care of the rest. And if you haven’t rebalanced since ’09, do it now.

Underweighting assets requires more work. Now, this goes beyond basic rebalancing to a tactical allocation model. You’ll actually lower your allocation in U.S stocks and raise your allocation in poorer performing assets or areas with a higher chance to outperform. Basically, you’re looking for undervalued markets. This requires a bit more work and vigilance. So if you’re not looking to put more effort into your portfolio, stick to rebalancing.

Go International

There are two areas that fit those tactical requirements: Europe and Emerging Markets. One is prepped to outperform and the other has simply become hated.

Europe

Europe is getting better. Europe, through international funds, already has a place in most portfolio allocations. Even if you own stocks, there’s a good chance the company does business there. So this should be no brainer.

The Euro economy rivals the U.S. even in a recession. Economies on the upswing make for good investments and Europe is just replaying what the U.S. went through the past few years. With signs that recession is ending, it’s more good news for Europe and European stocks.

- iShares MSCI EMU Index (EZU)

- Vanguard FTSE Europe ETF (VGK)

These two ETFs offer a broad, diversified exposure to European stocks and should be more than adequate for most long-term investors. You’re welcome to dig into individual countries to beef up your returns.

Emerging Markets

Hatred is the best way to describe how investors view emerging markets. We like hated markets. That means opportunity.

Here’s how it plays out. Many investors hate poor performing assets, so they sell low, locking in big losses. The more this happens, the more those assets become attractive. Good investors want to do the opposite – buy low, sell high.

Right now emerging markets fall into the buy low camp. Sure, they could still go lower. In the long run, there is a high probability these markets will outperform over the long term.

I covered several emerging market ETFs not too long ago (it was a subtle attempt to point out the opportunity). Here are those ETFs again:

- Vanguard FTSE Emerging Markets ETF (VWO)

- iShares MSCI Emerging Markets Index Fund (EEM)

- WisdomTree Emerging Markets High-Yielding Equity Fund (DEM)

The alternatives are individual country or continent ETFs if you have the time and energy for extra research. Just something to think about if you have the patience to wait and can handle the risks.