International and emerging market stocks underperformed U.S. stocks over the past 15 years. It wasn’t consistent every year. In fact, international led in three of those 15 years while emerging markets led in four. Still, it wasn’t enough to outpace the U.S.

So far, this year has been another exception. Through nine months, both international and emerging markets have outperformed both U.S. large and small caps by a wide margin.

The obvious question is: is this another one-off year or the start of a longer trend much like the one experienced during the early 2000s?

Which brings us to the first of several lessons from the returns so far this year:

- There’s more to investing than U.S. markets. Great US bull market runs, historically, are followed by periods of below average performance. In those moments, non-US stocks prove their worth. Maybe this is another one-off year or maybe it’s the start to a longer trend. The downside of uncertainty is why we diversify.

- Market returns can happen in short bursts. Just look at emerging markets, US small caps, or any number of country indexes in the past few months. Emerging markets jumped 18% over the four months from June thru September. All of the US small cap gains year to date occurred from August 4th to the end the September (the Russell 2000 total return index was 12,060 to start the year and ended August 4 at 12,055). That’s 10.4% in two months.

- Discipline to stay the course. Small caps dropped 21% from January to April after tariff announcements tanked the market. Small caps are up 39% since the April 8th low. US large caps fared better during the tariff rout, only down 15% but are up 35% from the same April 8th low. Panic selling is not a solution to long term investment success.

- DCA and rebalancing has its benefits. Dollar cost averaging (DCA) and a rebalancing strategy are two simple ways that investors can automatically take advantage of short-term poor performance in asset classes like those seen in US large and small caps earlier this year and be better off for it in the long run.

A quick note before the third-quarter highlights. The asset class, sector, international, and emerging market returns are up to date through September 30, 2025. Hit the links for each.

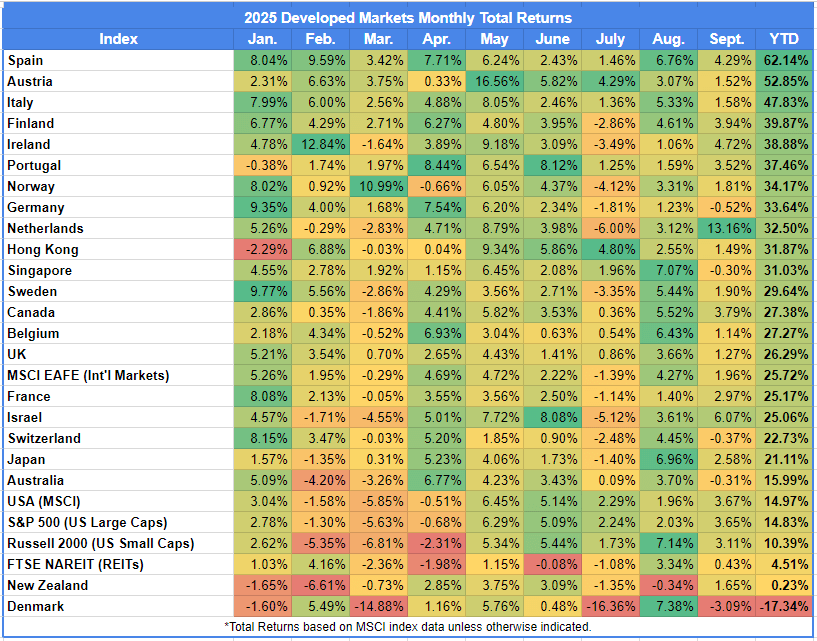

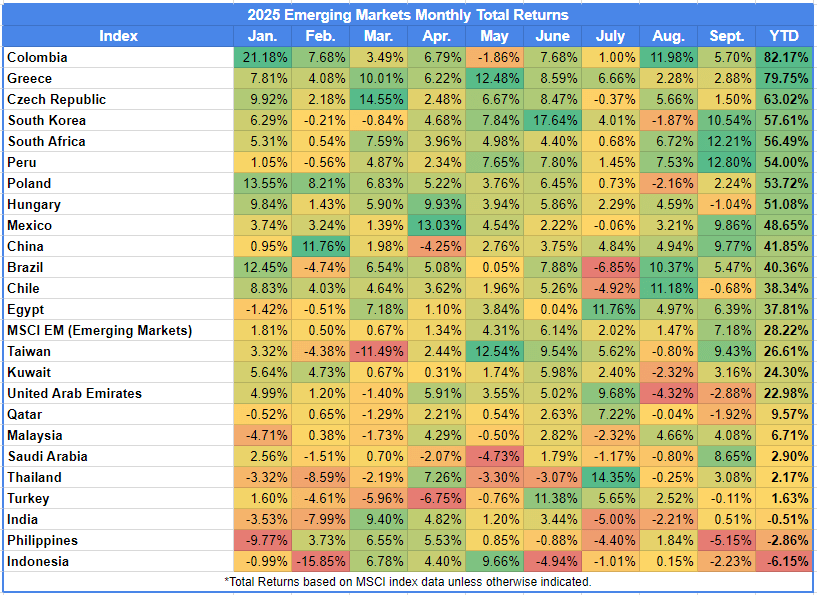

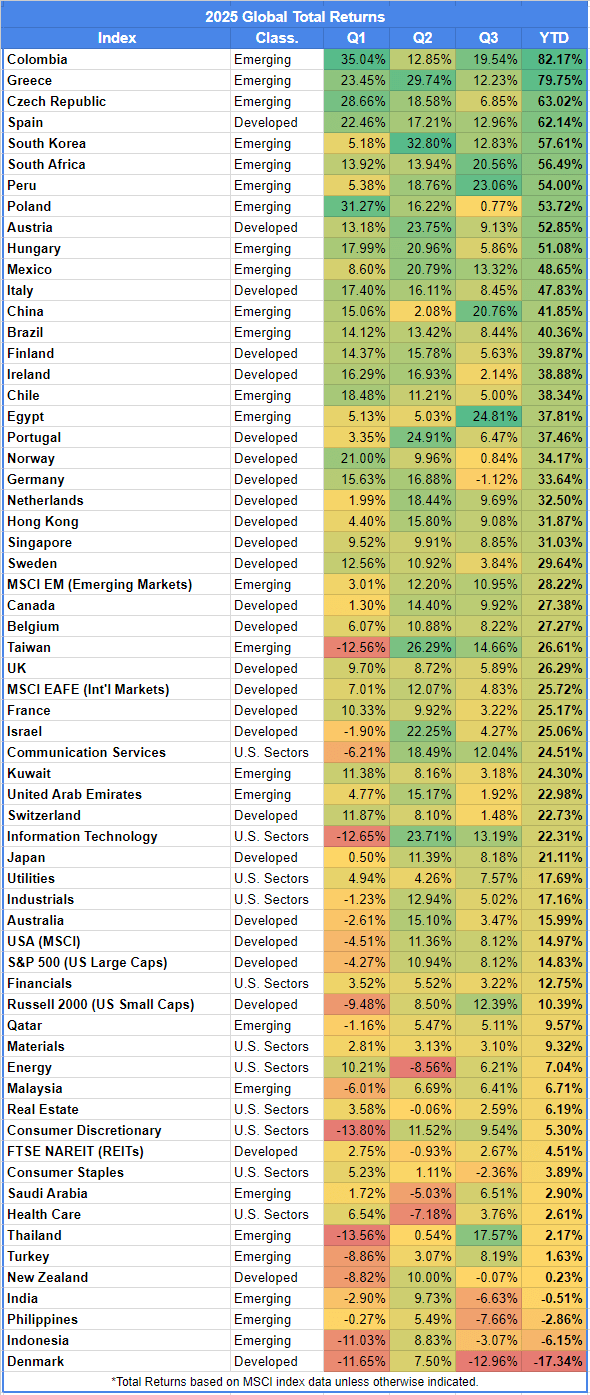

Four tables are below. The US sector, developed markets, and emerging markets performance broken down by month. The last table shows quarterly returns for all three.

Here are a few notable highlights:

- The big market story this year (besides tariffs) has been AI, Tech, and the magnificent seven. Interestingly, the seven largest companies are not all in the tech sector. Four are in the Info Tech sector. Two are in the Communication Services sector. One is in Consumer Discretionary.

- Both the emerging and international markets indexes have outperformed the US Info Tech, Communications, and Consumer Discretionary sectors to date.

- 31 (out of 46) international and emerging market countries have outperformed all three sectors this year.

- In fact, the emerging market and international market indexes have outperformed an equal weight basket of the magnificent seven through Q3.

- Consumer Discretionary is the worst performing sector of the three at 5.3% year to date. The other two sectors are the best performing US sectors this year at 24.5% (Comm Services) and 22.3% (Info Tech). All three sectors were the worst performing sectors in through Q1.

- The Spain, Austria, Italy, UK, Greece, and South Africa indexes saw gains across every month this year so far.

- The emerging market index also saw gains in each of first nine months this year.

- 35 countries have gains on the year in excess of 20%. 36 are outperforming the S&P 500.

- Only four countries have losses on the year. Denmark being the worst at -17%, mostly due to concentration risk. A heavy weighting in a single company, with a large loss this year, had an oversized impact on the index.

Related Reading: