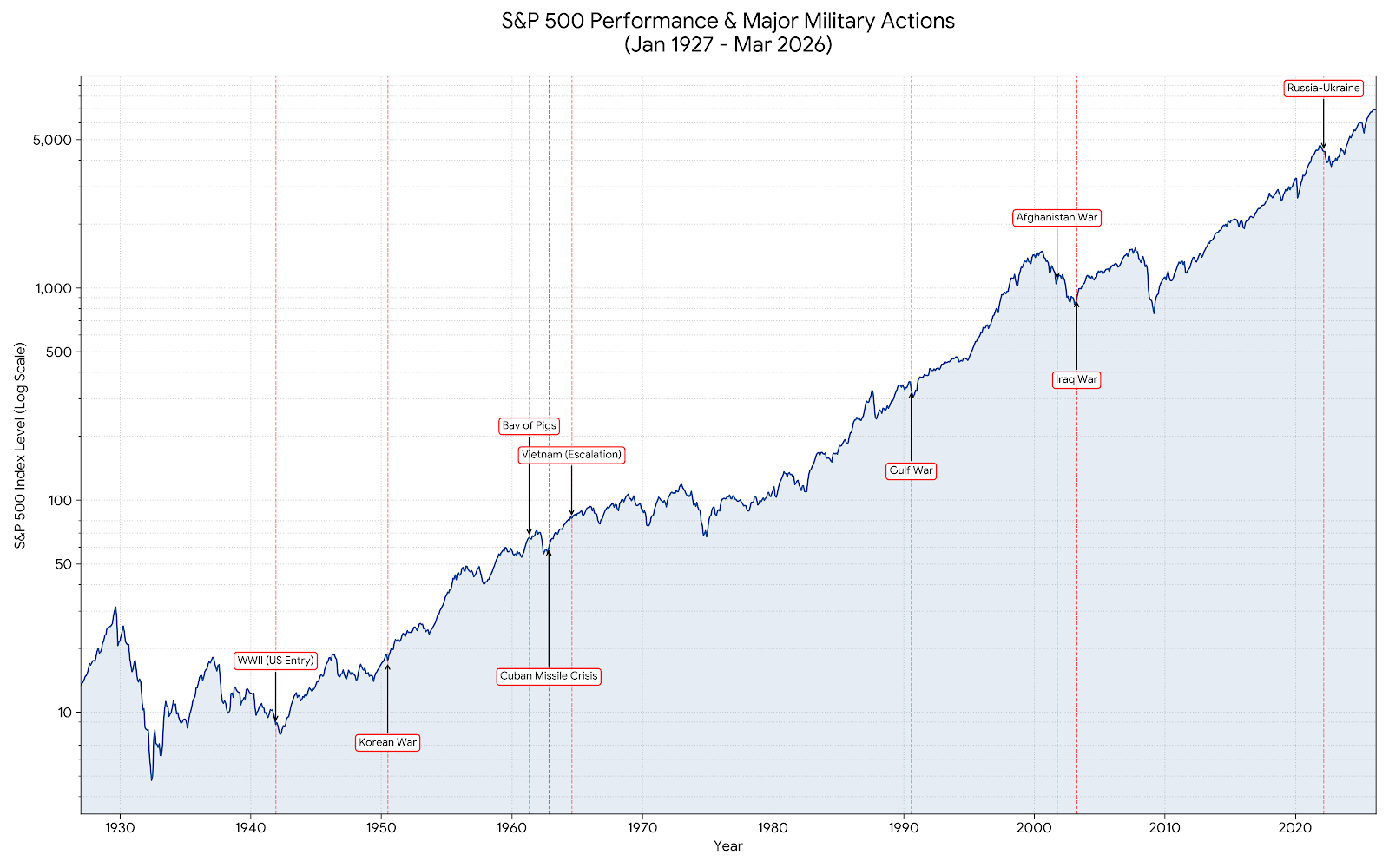

Alot of things must go right to perpetuate a massive fraud. It certainly did for Tino De Angelis and his salad oil swindle in the early 1960s.

How does someone commit fraud with salad oil, you ask? Tino started Allied, a vegetable oil refining business with the goal of becoming the industry leader. He needed growth to achieve that end. So, he borrowed money in a unique way.

Tino used Allied’s existing inventory as collateral for loans. Tanks full of soybean and cottonseed oil were pledged to secure loans. The initial loans came from exporters. Banks, brokerage firms, and more eventually became willing lenders because the warehousing receipts tied to Allied’s inventory carried the name American Express.

Tino scheme was simple. He only needed people to believe the vegetable oil existed, so he created that illusion. He built a network of over 70 tanks that allowed him to pump contents from one tank into another while inspectors checked the contents of a third.

And the contents? A few tanks held petroleum, gasoline, soap stock, and sludge. The majority held salt water…with a thin layer of oil floating on top. In the end, 1.85 billion pounds of inventory was unaccounted for!

Continue Reading…