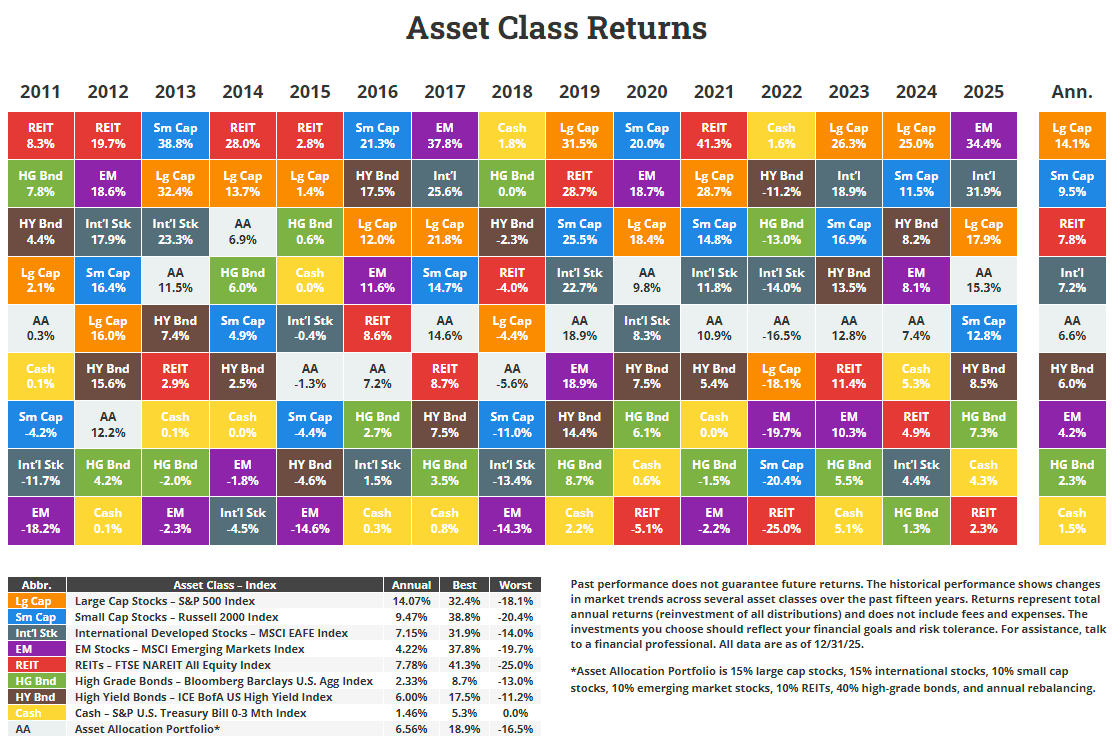

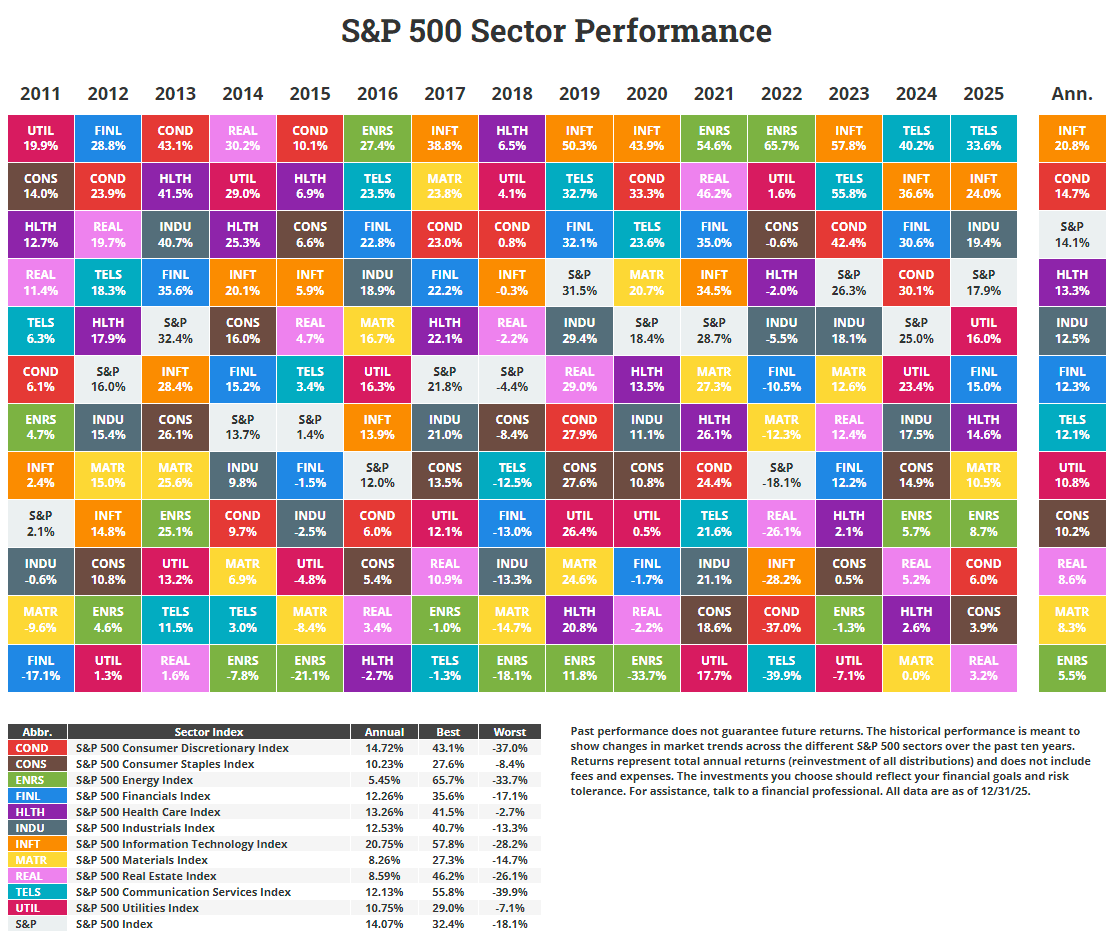

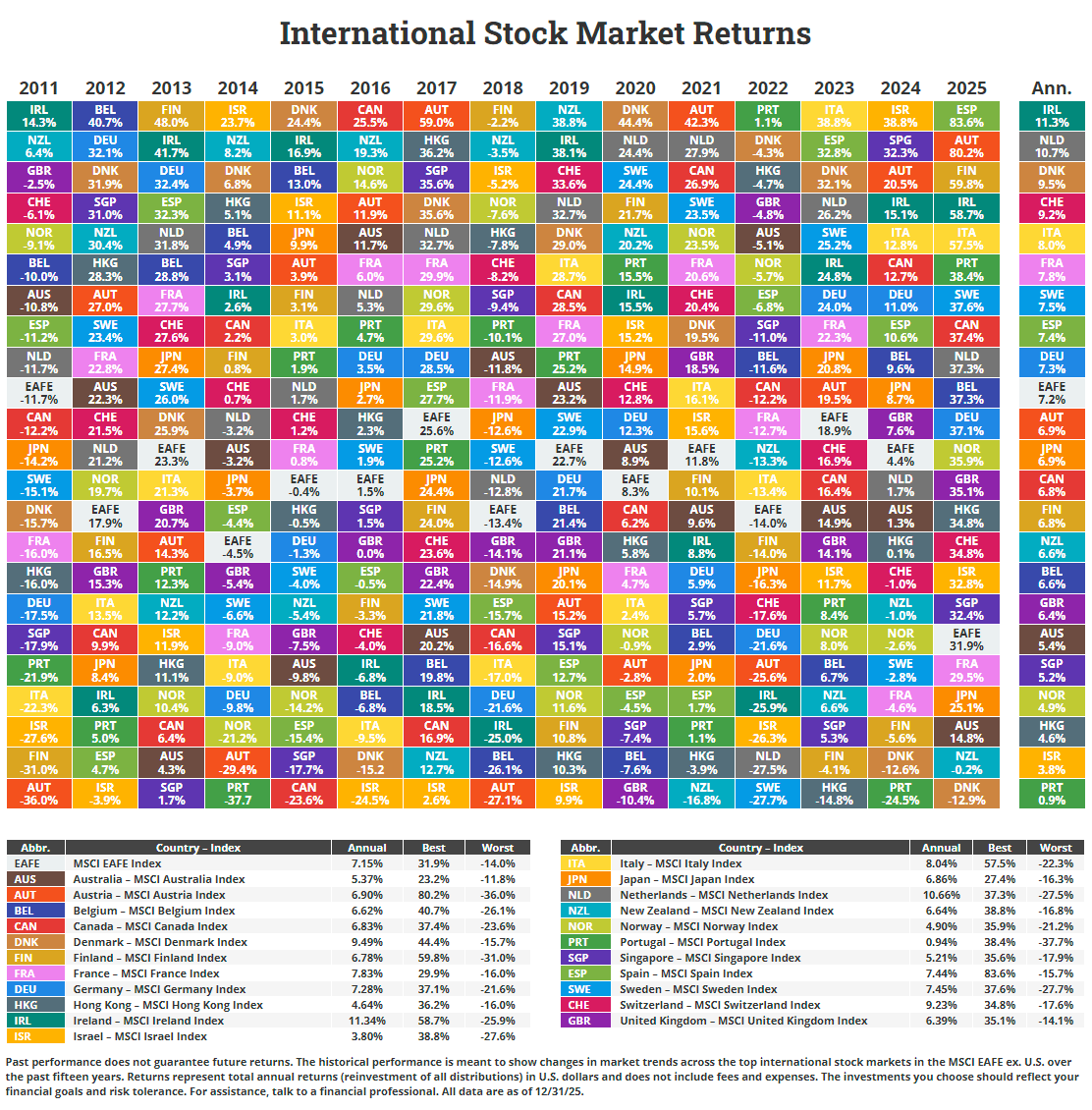

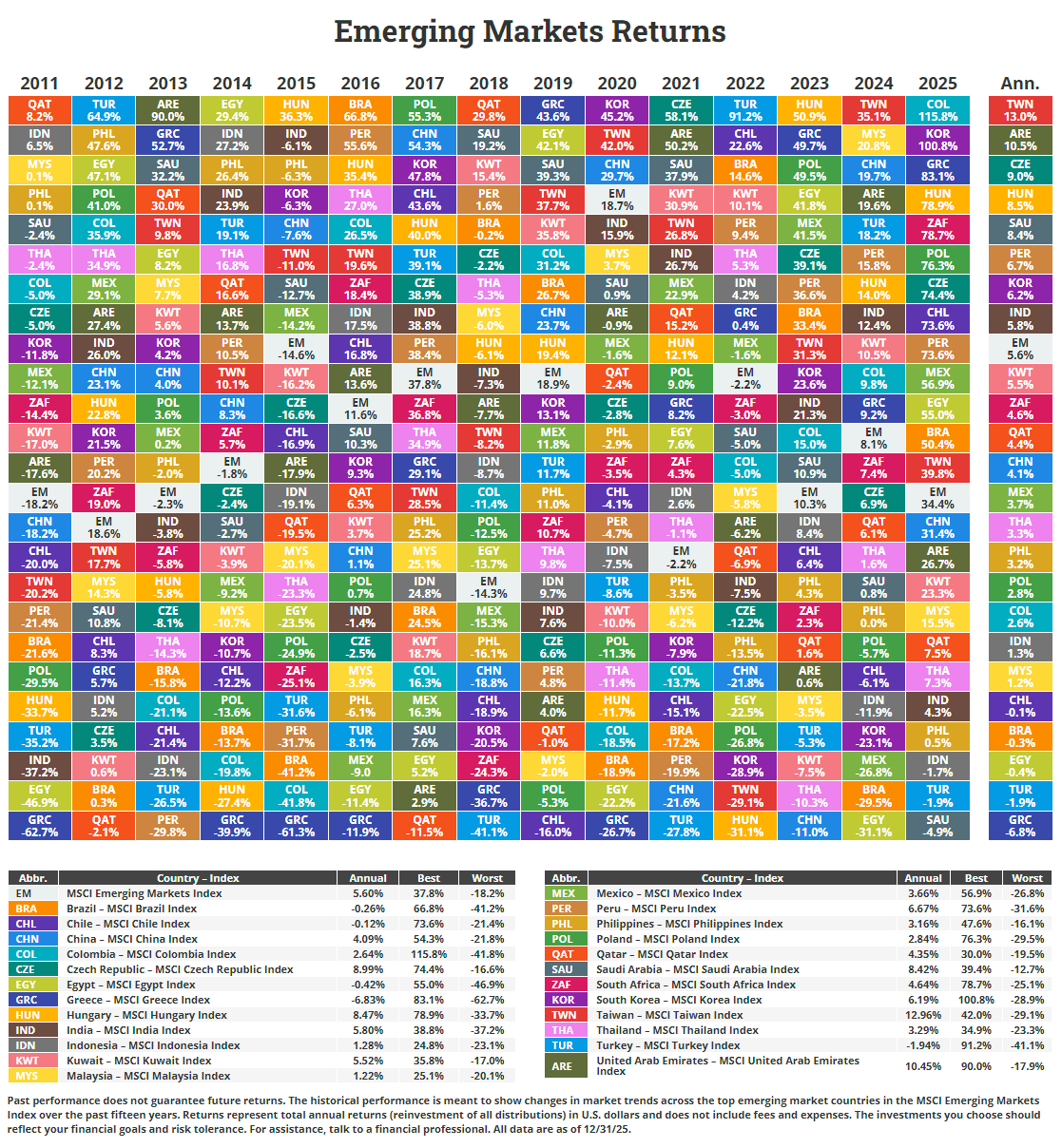

The asset class, sector, international, and emerging markets quilts are up to date for 2025. Links to the updated versions are below:

You can also download copies here or grab the images below (screenshots work too). The historical data is updated and available for download as well.

I’ll have the usual deeper dive for you next week.

For now, the lesson of 2025 is not a new one. A home-biased portfolio carries the risk of falling short of a more diversified allocation. That was true for 2025. Allocations into U.S., international, and emerging market stocks produced a better return than a U.S. only allocation.

Broadly, the major asset classes were positive on the year. Emerging and international stocks topped the list with total returns in excess of 30%. U.S. large caps finished the year at 17.9%. U.S. small caps earned 12.8%. High yield bonds, high grade bonds (U.S. Agg), cash (3-mo T-bills), and REITs were next, in that order.

All U.S. sectors were positive on the year too. Telecom, Tech, and Industrials performed better than the S&P 500. Energy, consumer-based companies (Discretionary and Staples) and Real Estate were the worst performing sectors, in that order, and the only sectors with single digit gains for 2025.

Globally, 42 of the 47 developed and emerging country indexes ended the year with gains. The Columbian market was the best at 115.8%. The Danish market was worst at -12.9%. A total of 17 countries saw market gains in excess of 50%!

So, yeah, it paid to be diversified. More to come.