The story of 2023 is one of alleviating the market worries of 2022. Higher inflation, higher interest rates, recession, and further market declines were predictions pushed for 2023.

Then again, there’s always something to worry about. Except, as is often the case, the last thing you have to worry about is what everyone’s talking about. Because the odds are good that those concerns are already priced into the market.

Unfortunately, the biggest risks are the risks we don’t think up. In other words, we build our portfolio to protect from surprises, not the common market concerns everyone expects.

So how did those 2023 worries fair?

1) Inflation Falls

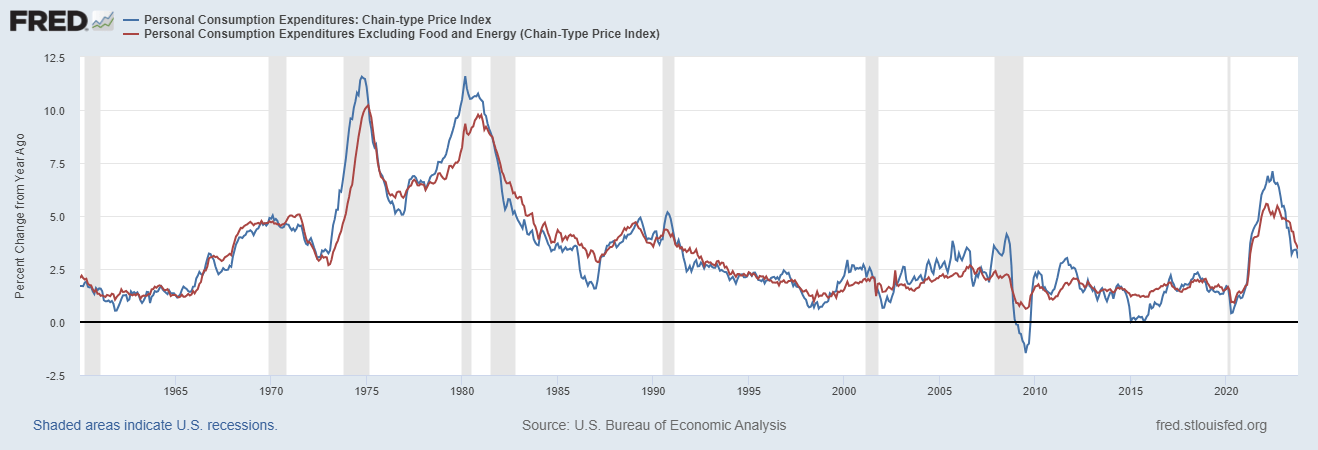

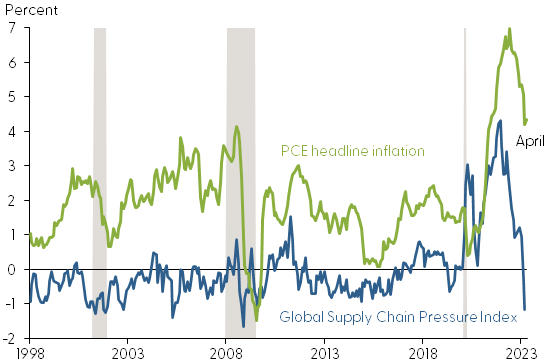

Inflation is subsiding. Both the PCE and PCE ex-food and energy have fallen below 4% year over year. Why?

The supply chain shock is subsidizing. The leading contributor to the inflation spike following 2020 was due to supply shortages because of global supply chain disruptions. Supply couldn’t keep up with higher demand. That is now easing as seen in the chart.

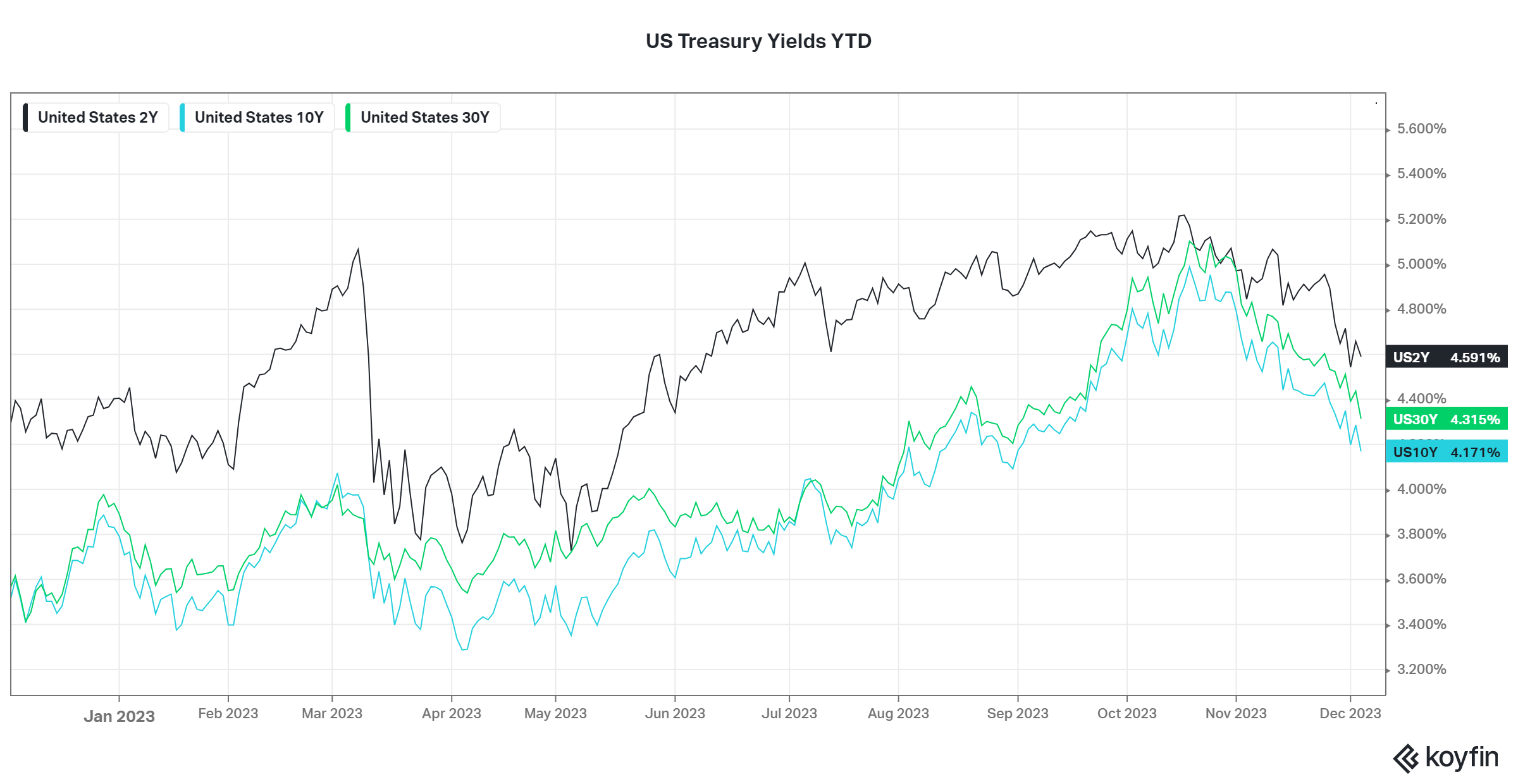

2) Interest Rates Stabilized

Treasury yields are up less than 100 basis points (less than 1%) since the start of the year. Sure, 2-year and 10-year peaked around 5% in October, but good economic news in November has seen rates recede slightly. More to the point, the extreme rate of change we experienced in rates last year, ended in 2023.

One word of note, that sharp drop in the 2-year in early March coincides with the Silicon Valley bank collapse that reminded everyone about the FDIC limits on their bank account. The drop is most likely due to panic buying that pushed bond prices higher and rates on those bonds lower.

Most importantly, today’s interest rates give you more flexibility when allocating your portfolio. I mentioned this while summing up last year too. Low rates forced investors to choose between higher-risk assets or lower returns. The current rates create a legitimate choice between 4+% treasuries or higher-risk assets. It allows for a margin of error in your portfolio that didn’t exist with historically low rates.

3) Recession that Wasn’t

It’s safe to say — so far — 2023 went without that predicted recession. The good news is those same people who predicted a recession for 2023 (and 2022 and 2021…) are repeating the same claims for 2024. Maybe it happens. Maybe it won’t. What we know is that the economic data has been better than expected. We also know (should know) that recessions are inevitable and hard to predict.

4) Market Rebound

Hint: Click the charts to supersize it.

The Dow, S&P 500, and Nasdaq continued their recovery from their October 2022 lows. The worst performers last year are the best performers year to date. And of the three indexes, the Dow is closest to its all-time high back in 2021, followed by the S&P 500, then the Nasdaq.

Breaking the market down by sectors has the Technology, Communications, and Consumer Discretionary leading the way. Those three were three of the four worst-performing sectors last year (the fourth being Real Estate). Energy has the worst return year to date. That said, it’s been the best-performing sector since 2021.

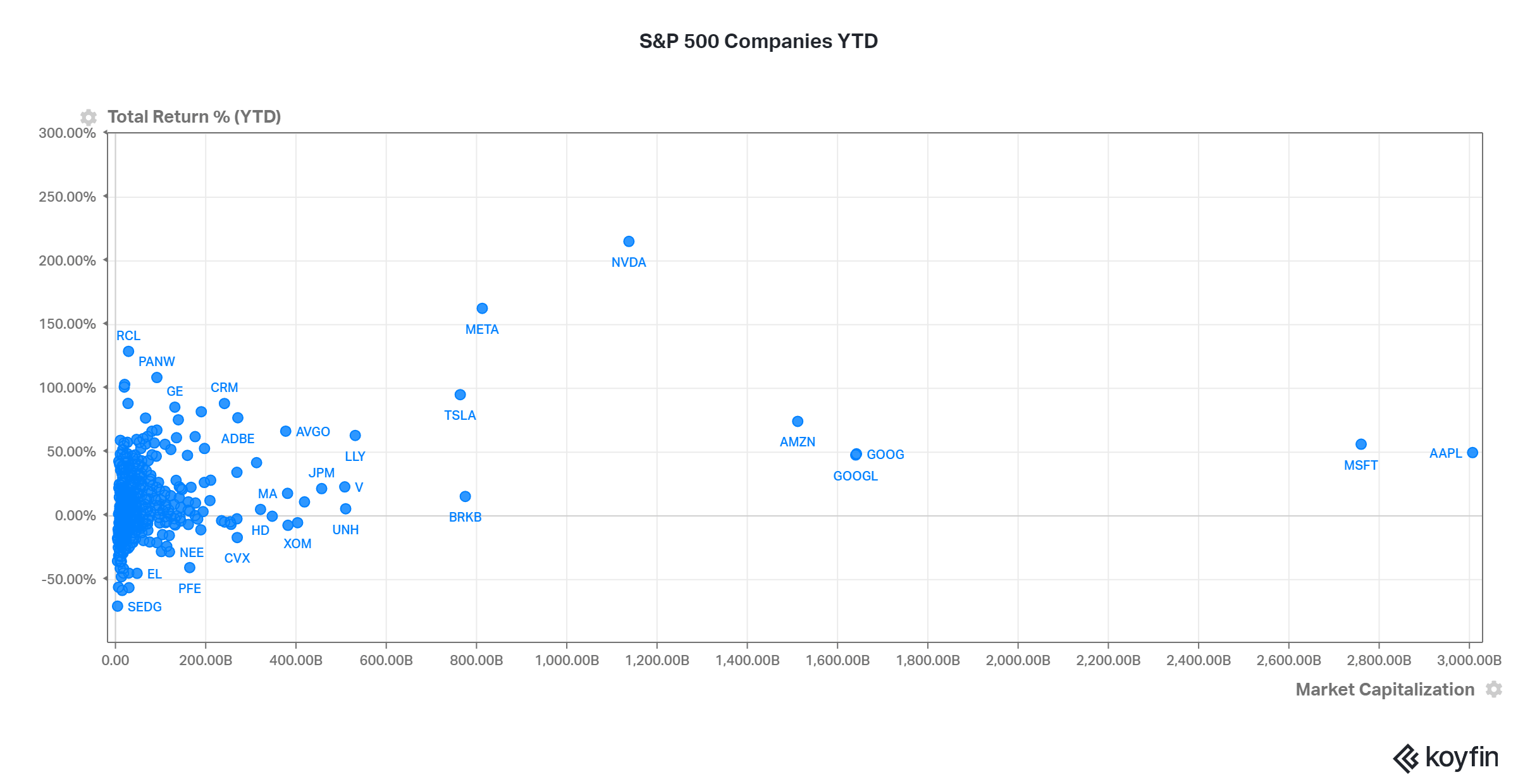

One of the bigger discussions this year is how the largest companies in the S&P 500 are driving the index’s performance. The chart above lays this out.

Of the eight largest S&P 500 companies by market cap, seven — Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, and Tesla — are outperforming the S&P 500. Those seven have year-to-date returns ranging from 47% to 215%, far better than the S&P 500. The one exception is Berkshire Hathaway with a return of 15% year to date.

Of course, those same seven companies were crushed in 2022 with losses ranging from -26% to -65% on the year, far worse than the S&P 500. Berkshire Hathaway, the exception again, was up 3% in 2022.

So no surprise, that the biggest companies have an outsized influence on the performance of a market cap-weighted index but even then, they don’t control its destiny entirely. The benefit of diversification is that winners more than offset the losers over time.

I can make up a long-winded story about why the market did what it did this year but the simple explanation is that the worries coming into the year were overstated and the stock market continued to recover. As is often the case, most market worries turn out to be less concerning long after the fact. 2023 is no exception.

Still, too many investors worry about the wrong things. The goal of investing is not to predict what interest rates or inflation will be two years out or to avoid the next recession. Trying to predict the economy is a fool’s errand.

The goal of investing is to build a portfolio you can stick with that holds a basket of good, growing companies over time but also holds bonds that protect it from unexpected risks that arise in the short run. The number of companies in that basket can be as big or small as your comfort allows. They can be from as many different sectors and countries as you choose.

Why? Because good, growing companies should be strong enough to weather the economic storms when they arise and bonds help offset the temporary declines in those companies that occur when the storms hit.

What matters is that you don’t try to jump in and out of that basket to avoid every potential economic problem on the horizon. Because there will always be background noise and fearmongers pushing scary scenarios that may (but not really) happen. Let others act on it. Emotional investment decisions are a common way to lose money.

Participating in the success of businesses is a great path to wealth. The best way to do that is uninterrupted.