Did you know you might be overpaying capital gains tax on investments because of tax rules that went into effect in 2011? Those new rules changed the way we report capital gains and losses on investments. Under the old rules, it was your job to report cost basis, that’s what you paid for the investment, to the IRS. With the new rules, it’s your broker’s or fund company’s responsibility.

Did you know you might be overpaying capital gains tax on investments because of tax rules that went into effect in 2011? Those new rules changed the way we report capital gains and losses on investments. Under the old rules, it was your job to report cost basis, that’s what you paid for the investment, to the IRS. With the new rules, it’s your broker’s or fund company’s responsibility.

Before the rules change, lets just say not everyone was truthful about their gains. The honor system doesn’t work well with taxes. Putting the onus into the brokers and fund companies’ hands add a layer of protection for the IRS.

Instead of number crunching your way to lower taxes at year’s end, you now need to calculate cost basis at the time of sale. That involves tracking your profits/losses, so you can pick the cost basis method that gives you the best tax savings for the year, without hurting you later on.

For those that don’t know, when you sell a portion of the shares you own, the cost basis method tells the IRS which of those shares are sold. The basis of those shares ultimately decides your gain or loss for the sale.

There’s one problem with all this – your broker or fund company preset a default cost basis method for you. That default method probably won’t give the best tax results when you sell shares. What you may not know is, you can change the default method to the one you want to use.

Why The Default Method Matters

When you open a taxable account with a broker like or a fund company, the default cost basis method is already set for when you sell shares.

The problem is twofold. The default method used by fund companies and brokers differs across the board and the method used by each is not the best solution for your tax bill each year.

Most fund companies have turned to the average cost method as the default setup. The majority of brokers, but not all, set FIFO as the default. Neither is good or bad per se because there is no single best method to use all the time. It depends on what you want to do from a tax perspective.

Cost Basis 101

Every time you buy shares of a stock or fund, whether it’s one share or 1,000 shares, that purchase is given a tax lot ID. You can have multiple tax lots in the same stock or fund.

If you buy 100 shares of XYZ fund, those 100 shares are given a unique tax lot ID. When you buy another 150 shares of XYZ fund, those 150 shares will be given a new tax lot ID. It doesn’t matter if you bought the 100 and 150 shares 1 minute apart or 4 months apart. Each purchase gets a unique lot ID.

When you choose to sell shares of XYZ fund, whether it’s one share or 249 shares, the cost basis method you choose has an impact on the amount of taxes you pay. If you choose to sell all 250 shares of the XYZ fund, the method of choice won’t matter because you’re selling all your tax lots at once.

That’s the simple version. But it can get complicated. For instance, take a mutual fund. After a year of monthly share purchases and quarterly dividend reinvestment, you’d have sixteen separate tax lots for one fund. Do that for several years and you can see how complicated things can get.

Make A Choice

There’s no simple solution to this either. The unpredictable future of taxes and share price makes it harder. That’s why we have tax planning – to choose the right cost basis method that helps lower your taxes now and in the future.

You don’t want to stick yourself with a higher tax bill in the future for the sake of lower taxes today. Nor do you want the opposite. The six methods to choose from each have its own pros and cons.

FIFO

FIFO (First-in, First-out) is the default cost basis method used by most brokerages when you open a new account. That doesn’t mean it’s the best method to use every time.

FIFO sells the oldest shares you own first. Because of this, it tends toward selling the longer-term tax lots. Long term capital gains (from shares held over 1 year) are taxed at a lower rate than short-term gains. In this respect, FIFO typically gives you a lower year-end tax bill. Until you run out of shares owned more than one year. Then you’re stuck selling shares that qualify as short-term and the higher tax rate that comes with it.

LIFO

LIFO (Last-in, First-out) is the exact opposite of FIFO. LIFO sells the newest shares you own first. Share that qualify as short-term (owned less than one year) are taxed at your income tax rates. By always selling the most recently bought shares first, you build up a sizable number of long-term qualified shares.

For anyone in the higher tax brackets, LIFO is not the best option.

Highest Cost

The highest cost method selects the tax lot with the highest basis to be sold first. Put another way, the shares you paid the most for, are sold first.

One thing to keep in mind, the highest cost method doesn’t consider the length of time you own shares. It’s designed to sell shares that give the lowest gains or biggest losses first. Short or long-term is not considered.

In essence, the highest cost focuses on harvesting losses first, before taking gains.

Lowest Cost

The lowest cost method selects the tax lot with the lowest basis to be sold first. In other words, the shares you paid the least for, are sold first.

Like the highest cost, length of time is not considered when choosing which lot to sell. This method is designed to maximize gains regularly culling capital gains at each sale. It’s used most often to take advantage of realized losses that can be offset by large gains or to harvest gains now in order to prevent a bigger capital gains hit in the future.

Average Cost

The average cost method is only available for mutual fund shares. That’s why it’s typically the default method for fund companies. The average is figured from taking the total price paid for all your shares, then divided by the total number of shares owned.

This may seem like the easiest way, but again, it’s not the best. There is one caveat. Once you use sell shares of a mutual fund using the average cost method, any existing shares are locked into that method too. However, the method can be changed for any new shares purchased after that sale.

Specific Lot

Instead of using the other method, a specific lot lets you handpick exactly which lots you want to sell. This method is more hands-on than the rest since you pick which tax lots get sold each time you sell shares. It’s also the most tax-efficient because it offers the best chance to control your tax bill each year.

By handpicking a specific lot, you can adjust your yearly long and short-term capital gains and losses on every sale. The specific lot method offers the best financial outcome since it forces you to be actively aware of your investments and tax liability.

Make The Change

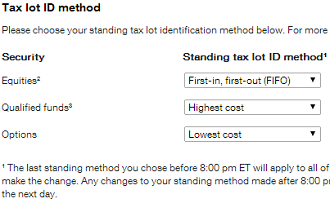

It’s easy to change the default setting on your taxable accounts. Just tell your broker or fund company which new cost basis method you want to use. You can change the method as many times as you like. Brokers should allow you to make changes online.

I changed the default setting for my TD Ameritrade brokerage account under Client Services > My Profile > General Settings. With TD Ameritrade, you can also select the method when you place an order.

But know that once shares are sold, there’s no way to go back and retroactively make changes. It’s best to set your method of choice now before you start selling off shares. This way you won’t unknowingly lock yourself into a bad decision.

Regardless of which method you choose as your default method, I recommend tracking your gains and losses throughout the year. Because it’s important to use the right cost basis method to help lower your taxes now and in the future.