In 1992, Seth Klarman warned investors of being too greedy toward yield. He watched investors chasing anything that came close to the high yields they once earned in the 1980s.

Well, history may not repeat but it does rhyme.

A similar thing has been happening for a few years now. This time around, I doubt greed is the driver. Rather, fear of not earning enough is pushing investors into higher-yielding assets. Junk bonds, emerging market bonds, and stocks look more attractive because the assets investors once relied on for yield fall way short of their needs.

Howard Marks explained the problem perfectly in a recent interview:

This market is not built on some euphoric view of the future, but mainly on the unwillingness to accept zero or negative returns on cash and safe instruments. It’s based on the view that there is no alternative: people are afraid to be out of the market. But then again, a perceived lack of alternatives is not a good argument for chasing yield and taking big risks. That’s why I think this is the time to turn cautious.

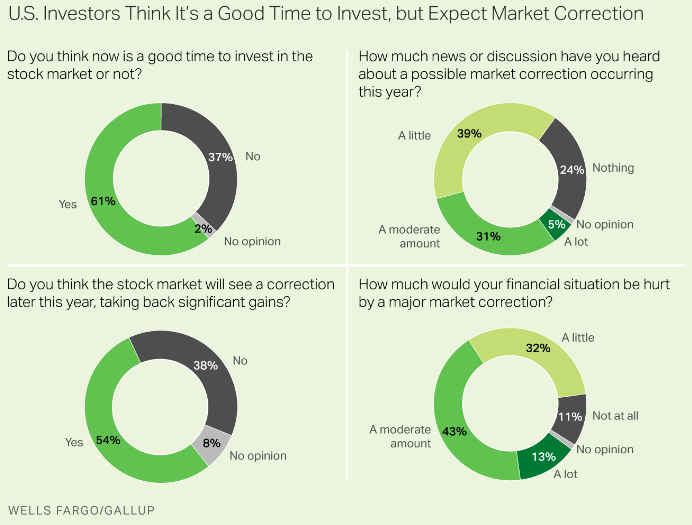

It looks like the current sentiment echoes his thoughts:

- 61% believe it’s a good time to invest in stocks

- 70% have heard a correction is possible in the news

- 54% believe a correction is possible

- 88% would be hurt, in some way, by a major correction

Investors are taking the risk anyway because they believe they have no other choice and/or they believe they can get out in time. I wouldn’t put too much faith in the latter. And sometimes when you’re faced with no alternative, it’s better to be safe, than sorry.

Which makes me ask a few questions not in the survey: How will they react to a correction? Will they suffer through it and do nothing? Will they be driven to act? Will fear drive their actions or will they be forced to sell?

When everything is going well, why have money in cash and bonds that yields so little, when stocks (and high-yield bonds) have performed so well? Because everything is relative when things are going well and investors need to earn a higher yield.

In the investment world, people always compare one asset relative to the other… But what about the absolute judgment when we realize that they are both overpriced? You can’t eat relative returns. — Howard Marks

And because the importance of having a low-risk allocation is never more apparent than during a correction.

This “Look what I could be making” attitude gets investors into trouble. Thinking that way leads to chasing returns, taking too much risk, and almost always result in bigger losses than a portfolio can handle.

Large losses are forever, and a 50 percent loss requires a double the next time up just to get even. Large losses are almost always caused by trying to get too much and taking too much risk. — Charles Ellis

Opportunity costs in a rising market always seem high (while the risks seem low). Since the stock market ends higher about 70% of most years, holding cash and bonds that earn next to nothing usually look like the wrong choice.

But that’s the wrong way to look at it. You can’t just consider what you could gain, you have to weigh it against what you’re giving up.

As an investor, you have to deal with two risks: The risk of losing money, and the risk of missing out on opportunities. It’s the job of a good investor to balance the two: You invest, but with caution… I think it’s better to turn cautious too soon rather than too late. Most people can’t think of what might cause trouble anytime soon. It’s precisely when people can’t see what it is that could make things turn down that risk is the highest… It’s always the things we don’t know about that really bite us in the end. — Howard Marks

***

Unless they are deluding themselves, investors understand that to achieve incremental yield above that available from U.S. government securities (the “risk-free” rate), they must incur increasing levels of principal risk. There is no risk-free yield enhancement on Wall Street. The painful result: Higher risk investments often erode one’s capital and produce lower returns — the worst of all investment worlds. Higher-returns-for-higher-risks only applies on average and over time. — Seth Klarman

When weighing opportunity cost you have to consider why you allocated money to safer bonds or cash in the first place. Both play a specific role that stocks (and high-yield bonds) don’t offer. Cash and bonds help to temper losses, temper your emotions, and can be a source of funds in an emergency.

Often, both can seem like wasted opportunities but have a unique way of providing comfort when you need it the most.

Source:

Klarman: Don’t Be a Yield Pig – Forbes 1992

Marks: Nobody Knows What Will Happen

Ellis: Investing Success in Two Easy Lessons – CFA Digest 2005

U.S. Investors Expect Market Correction – Gallup

Related Reading:

Seth Klarman on Chasing Yield

100-Year-Old Investment Advice