Much of the discussion around investing involves managing costs. Taxes need to be part of that talk. Like fees and expenses, dividend and capital gains tax eats away at your returns.

Much of the discussion around investing involves managing costs. Taxes need to be part of that talk. Like fees and expenses, dividend and capital gains tax eats away at your returns.

Any time your investments make money, taxes aren’t far behind. To make it easy on us, Congress whipped up a simple complex tax code for income, dividend, and capital gains tax rates. Lucky for us, that tax code can change on a whim, making it worth staying updated on.

Before we go any further, dividend and capital gains tax are for money invested through taxable accounts only. Taxes on investments are a moot point when dealing with retirement and other tax advantaged accounts. You can buy and sell all day without worrying about the tax consequences, though I don’t recommend it.

Anytime you buy, sell, or make money inside of a taxable account you win a tax form at the end of the year. The IRS has tax forms for every type of investment income to make your annual tax prep easier.

The end of the year is a typical time for you to do a financial review, decide the fate of your investments, and deal with any tax issues. Since the cost basis changes from a few years back, you need to make tax decisions at the time of the trade. If taxes aren’t part of your thought process before a transaction is made, it needs to be now. Here’s a complete guide on cost basis to get you caught up.

How Your Investment Income Is Taxed

Before you can do any tax planning around investments you first need to know what gets taxed, why, and by how much. There’s two separate issues to discuss:

- How your marginal tax rate plays a role

- How the tax code defines each type of investment income

Your marginal tax rate decides your investment tax rate. Anytime you can drop into a lower tax bracket, you not only pay a lower tax overall, you might significantly lower your dividend and capital gains tax rates.

This is why dividends, and to a lesser extent long-term capital gains, are part of an income investment strategy and why Buffett pays a lower tax rate than his secretary. When the bulk of your income is from dividends or long-term capital gains you pay a lower effective tax rate.

For us mere mortals this might seem like a strategy built only for the super rich, but it’s not. Something as simple as adding to your 401k lowers your taxable income, can drop you into a lower tax bracket, and lower your investment tax rates too. A little planning and foresight can have a big impact when you’re tax averse.

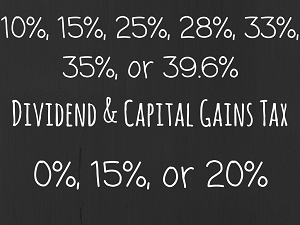

Below are the dividend and capital gains tax rates for each income tax bracket. The rates you pay are based on your marginal tax rate which you can find here.

| Income Tax Rate* | Long-Term Capital Gains Tax Rate | Qualified Dividend Tax Rate |

| 10% | 0% | 0% |

| 15% | 0% | 0% |

| 25% | 15% | 15% |

| 28% | 15% | 15% |

| 33% | 15% | 15% |

| 35% | 15% | 15% |

| 39.6% | 20% | 20% |

*Short term capital gains and ordinary dividends are taxed at your marginal income tax rate.

Refresher on Each Investment Income

Interest

Interest income is the easiest to deal with since almost all interest is taxed as ordinary income. Interest you earn from checking, savings, and money market accounts, CDs, bonds, and bond funds are all taxed at your marginal tax rate.

There are exceptions. Municipal bonds are exempt from federal tax and U.S. Treasuries are exempt from state tax.

Dividends

I’ve already discussed how the IRS defines each type of dividend. Yes, there’s more than one.

Here’s the short version.

Every dividend is ordinary unless it meets the three IRS requirements that qualify it for the lower tax rate. The most important is the holding period, which says you must own the shares for at least 61 days, including the ex-dividend date. Long term investors shouldn’t have any problems with this.

Final note: Not all dividends are real dividends. The term gets loosely used to cover anything from capital gains distributions from mutual funds, interest on a savings account, dividends from a REIT, and more, that the IRS considers non-qualified dividends. Know the tax consequences of an investment before you get into it so you can invest your money efficiently.

Capital Gains

A capital gain, in its simplest form, is what you get when you sell an investment for more than you paid for it. If you sell it for less than you paid, you get a capital loss. When I buy one share of an index fund for $20 and sell it for $30, I have a $10 capital gain, which I have to pay tax on.

The capital gains tax you pay depends on how long you owned the investment:

- Short-Term Gain – gain from investments sold inside of one year of the purchase date

- Long-Term Gain – gain from investments sold one year after the purchase date or later

- Short-Term Loss – loss from investments sold inside of one year of the purchase date

- Long-Term Loss – loss from investments sold one year after the purchase date or later

The tax code lets you use capital losses to offset gains – known as tax loss harvesting. As you might guess, it involves selling losing investments to offset gains from the year and avoid higher taxes.

The rule of thumb on capital losses is – capital losses first offset gains of the same type, then gains of the other type, and lastly, your income (up to $3,000). You can use any leftover capital losses to offset gains (or income) in future tax years.

You can use the same concept to harvest gains today to avoid higher taxes in the future. For example: anyone in the 15% tax bracket, who knows they’ll have a higher income next year, would pay a long-term capital gains rate of 0%, which is better than anything they’d pay in the future.

Final note: Essentially, capital gains grow tax-free until you sell. Keep that in mind before selling anything, especially shares you might want to buy back later. The price you sell at could be the last time you see that price again. Be aware of the 30-day wash sale rule before using any tax avoidance tip.

One Last Note

As if this isn’t enough, there’s the Net Investment Income Tax. That’s the 3.8% Medicare surtax added in 2013 from Obamacare. High income earners need to consider that complicated mess when tax planning their income and investments or get a qualified tax pro to decipher it for them.