One of the more confusing tax forms for investments is form 1099-B. Tax lingo is part of the cause. It’s like a foreign language at first sight. The tax code, and changes to it, cause the rest. It’s up to you to decipher what the 1099-B says.

Brokers and fund companies send form 1099-B when you buy or sell an investment, like shares of a mutual fund or stock. The form is a record of those transactions. When you plug the information into a Schedule D, you and the IRS can figure out your capital gains or losses for the tax year.

Of course, you owe taxes on capital gains, either short or long-term capital gains tax, based on how long you owned the investment. However, capital losses are used to offset gains or income and lower your tax bill.

A good accountant or tax software figures out what you owe, if anything, each year. I use TurboTax because it downloads the forms directly from my broker. You should still understand Form 1099-B and how the capital gains tax works since planning ahead can save you money.

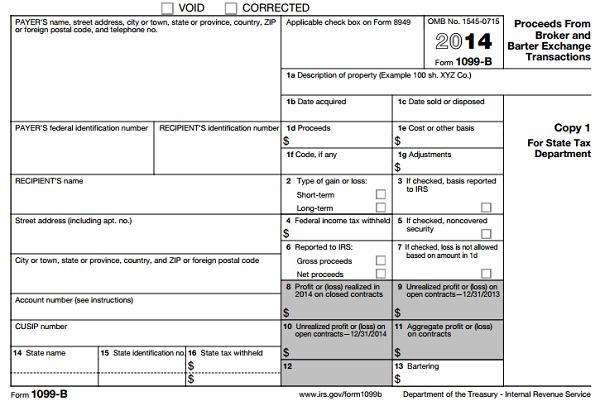

Form 1099-B

The tax code for reporting capital gains and losses is tricky. Here’s the simple version.

When you buy shares of a stock or fund, the price you pay, plus any transaction costs, is known as the cost basis. When you sell those shares, you subtract the basis from the amount of the sale to find out if you have a capital gain or loss. This guide on cost basis covers it in-depth.

In the real world, most people make semi-regular transactions, like buying mutual fund shares monthly or quarterly. Each purchase is a separate transaction, a separate cost basis for you to track, and it’s own unique tax situation when sold. After a few years, it’s easy to see how things get confusing fast.

If you buy shares through a broker there’s a good chance your 1099-B won’t look like the form below. Brokers often include it in a consolidated form 1099, along with other 1099s (DIV, INT, etc) wrapped together. Your broker might break the 1099-B part into sections.

For me, TD Ameritrade breaks it into three sections: short-term closed transactions, long-term closed transactions, and open transactions. I’m sure other brokers do something similar.

The left side of form 1099-B has the payer’s and your personal information – name, address, tax payer ID number or social security.

Then there are 22 boxes used to report tax information. Not every box will be filled out. Remember, 1099-B reports purchases and sales. If you don’t sell anything, then there’s nothing to report in those fields.

Note: Some investments may not have purchase information. The cost basis reporting rules were changed to include purchases of stocks in 2011, mutual funds and DRIPs in 2012, and other investments like bonds and options in 2014.

Box 1a – g

The first section covers information about each individual purchase or sale. Box 1a describes the investment, for instance, the number of shares, the ticker symbol, and the company’s or fund’s name. The date you bought the investment is in Box 1b.

Box 1c shows the date you sold it, the trade date. The amount you sold it for, minus any transaction costs, is reported in Box 1d.

Box 1e reports the cost basis of the investment sold, which you use to figure out your gain or loss.

There might be a code listed in Box 1f, because of the sale. For instance, the letter “W” stands for wash sales. If that’s the case, adjustments are reported in Box 1g. In the case of wash sales, the adjustment offsets any capital loss.

Box 2 – 4

The type of gain or loss is reported in Box 2. Short term is used on investments sold in less than one year. Anything sold one year or later is considered long-term.

You use capital losses to offset gains or your income. The rule of thumb is – capital losses first offset gains of the same type, then gains of the other type, and lastly, your income.

Box 3 tells you whether the cost basis was reported to the IRS.

Any federal tax withheld is reported in Box 4.

Box 5 – 7

These three boxes of the 1099-B help give more detail depending on the investment. Most of the time these are only used for unique situations.

Box 5 reports the sale of a noncovered security. A security is “noncovered” because it was bought before a certain date:

- shares of stock bought before January 1, 2011

- shares of mutual funds or DRIPs bought before January 1, 2012

- other securities (debt, options, futures) bought before January 1, 2014

Because of this, the cost basis isn’t reported by your broker or fund company. Though, you’re still responsible for reporting that information to the IRS on your tax return.

Box 6 shows the type of proceed reported. This will almost always be checked as gross proceeds. The one exception is – if your broker uses option premiums to reduce gross proceeds.

Box 7 will be checked if you received cash, stock, or other assets for stock you owned due to an acquisition or change in capital structure. If so, you can’t take a loss on those proceeds.

Box 8 – 11

These four boxes on the 1099-B only handle option, futures, and currency contracts. These will be blank if you don’t dabble in those investments. But for those that do, I’d recommend a good CPA. Here’s how it breaks down.

Box 8 reports profit or loss on closed contracts in the tax year.

Box 9 represents the unrealized profit or loss on open contracts at the end of the previous tax year. This is used to adjust any gains or losses on the year. Also, it would have been used on your prior year’s tax return.

Box 10 is the unrealized profit or loss on open contracts for the tax year.

Box 11 shows the aggregate profit or loss on contracts for the tax year. This amount is equal to Box 8 plus Box 10 minus Box 9.

Box 14 – 16

The last three fields are for state information. Box 14 lists the state. That state’s ID number goes in Box 15 and any withheld state taxes are reported in Box 16.