In one volume in the 30 volume set that makes up The Collected Writings of John Maynard Keynes lies practically everything you need to know about Keynes the investor. The entire volume is a collection of economic articles and correspondence, but it’s the first chapter that is the most informative.

That’s where you learn about his performance history both personal and professional, his economic views around some major historical events, and how he thought about investments and markets at the time.

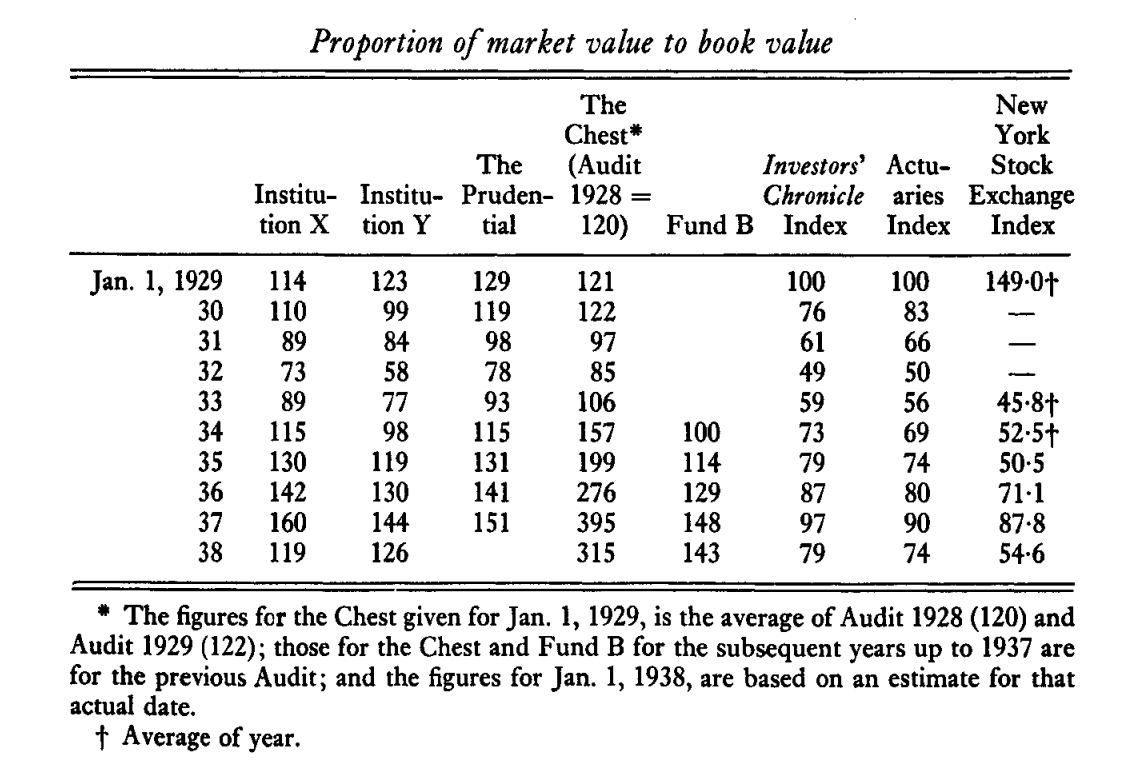

The history alone makes it interesting. But because it’s Keynes, that chance to critique an economist’s investment performance makes it appealing on another level.

Arguably he makes it difficult to do. He didn’t have a great start but he learned quickly and finished strong…for the most part. His professional track record was great, running the Chest Fund and advising for two insurance companies and several investment trusts.

His personal account was easier to criticize, as the first lesson shows. Continue Reading…

Buy the Book:

Buy the Book: