A successful plan to save more money is very straight forward. Set aside a decent chunk of your income early and let the power of compounding grow it over time. This doesn’t always go as planned. Other obstacles get in the way, like paying off debt and instant gratification (buying things you really don’t need).

A successful plan to save more money is very straight forward. Set aside a decent chunk of your income early and let the power of compounding grow it over time. This doesn’t always go as planned. Other obstacles get in the way, like paying off debt and instant gratification (buying things you really don’t need).

Those obstacles are why the personal savings rate sits below 5%. The guru’s say to save 15% of your income and live off the rest. That’s a big difference between reality and what’s recommended. That means most people will fall short of their retirement needs, unless they plan to save more money now.

For that to happen, changes need to be made. If you’re not saving 15% already, try it. It hurts at first, like ripping off a band-aid. Eventually the pain stops and you get used to it.

However, a big leap to 15% might shock some people into doing nothing. It shouldn’t. Given that alternative, saving anything is better than a self-inflicted financial coma.

Try 1% More

The other option for those pain averse folks inclined to slowly peel off the band-aid, or worse leave it till it falls off – start slow and gradually step up your savings.

Start with 1% more. It’s a small number anyone can budget around. That’s $38 a month for someone making $45k per year. It’s not much, but little numbers grow up to be big numbers when invested carefully. With enough time, that 1% has a decent impact on your retirement fund.

What About Saving 1% More Each Year?

Saving 1% is a good start, but to really save more money, a 15% savings rate is the first step to a larger goal. Remember, 15% is the recommended rate. To get there, why not save 1% more each year? By gradually increasing your savings, you ease yourself toward that goal. Once you reach 15%, why stop there?

Put It To The Test

It’s easy to say save 1% more and call it a day. Instead, I whipped together a spreadsheet to test it base on some basic assumptions:

- $45,000 starting salary

- 6% savings rate

- 3% annual salary increase

- 6% expected annual return

- 30 year time horizon

- Maximum 25% savings rate

Here’s the reason behind these numbers. In 2013, the average starting salary for college graduates was roughly $45,000, an achievable number for anyone. The typical 401k company match, if there is one, ends at 6% (any match is not included in the chart totals below), and it’s not far from the personal savings rate. A 3% annual salary boost is a worst case scenario where your income only keeps up with inflation. A 6% expected return is conservative. I capped the 1% increase per year at a 25% savings rate. This saving is done inside a 401k or IRA to take advantage of tax-free growth.

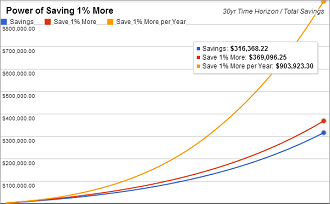

Here are the results.

Anyone interested can double check my work and play around with the numbers. If you find errors, let me know. You can adjust income, savings rate, annual salary increase, expected return, and savings rate cap. Go here, go to File, then Make a Copy, click OK, and it’s yours.

It’s no surprise that 1% more per year is so far ahead. It shows that if you’re not saving enough now, you can make small changes, gradually save more money, and still build a decent retirement.

Understand this is a conservative outcome. You can adjust the numbers to fit your situation. Though, you should focus on the areas you can control. Things like how much you save or how long you save are very controllable. A proactive approach toward saving more money upfront will have a bigger impact than anything else.

As your pay increases, earmark most of that toward savings. Just because you earn more doesn’t mean you should spend it all. Find a balance. You can automate this process. Use a savings account, your 401k, and an IRA (here’s a list if you need one) to funnel any extra savings towards.

Don’t assume investment returns will make up for a shortfall. Your expected return has limits. Yes, you might get higher returns in the future. You may not. The rise of index funds shows most people are content with average. Don’t stretch the truth by expecting more than that.

That said, poor decisions and emotions can derail average returns. You can avoid this. Build an asset allocation you’re comfortable with for the long term rather than reaching for the highest returns year after year.

Conclusion

A gradual approach to saving more money isn’t the most efficient way to retirement. There’s an opportunity cost to slowly raising your savings rate. You miss the early power of compounding. A better scenario might start at 10% or 15%, with a gradual increase from there.

But don’t overlook it either. Given the time, an extra 1% each year still makes a big impact. Once you do retire, you can draw more money from that bigger lump sum. In essence, by saving 1% more now, you give yourself a raise in retirement.