Anyone expecting a repeat of last year’s performance has to be disappointed. Global stock markets left much to be desired for the first half of 2018. Of course, markets can crush high hopes sometimes.

Usually, when that happens, bond markets offer a little recompense. That didn’t happen over the last six months. The few bond indexes I track for the asset tables (and many others) have all performed worse than 3-month T-Bills YTD.

That shouldn’t be a surprise though. Broadly, global stock markets have performed well since 2008. That wasn’t going to continue forever. And it’s hard to squeeze a high return out of low-yield bonds. Those two things combined are enough to reset expectations for the next several years.

The brings me to a few ultimate unanswered questions. How do investors react if low expected stock returns materialize in a low bond yield world? How many “long-term” investors stick with their strategy? Will investors take on more risk in the hopes of getting a higher return? Are they prepared if they’re wrong? Will they accept low or negative returns over the next few years?

Of course, how the second half of the year plays out is hardly certain. Maybe the next six months surprises to the upside.

I think the best way forward is to expect sub-par returns and adjust your saving (for non-retirees) or spending (for retirees) accordingly. There are times to be optimistic but that usually works better at the start of a bull market.

Anyways, a few brief comments before diving into the data (links to the updated tables are below along with YTD returns on everything, ranked highest to lowest):

- The S&P 500 had 1 losing year since 2003 when dividends are included. Tell anyone that’s how things would turn out after 2008 and they’d be shocked. Not sure if it’s over yet, but it was a surprisingly great run.

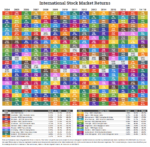

- Colombia and Finland were the only countries with double-digit returns over the past six months. I bet nobody guessed that!

- 13 countries finished the first half of 2018 positive. 34 countries finished the first half in the red.

- Consumer Discretionary sector unseated Tech as the best performing sector (Tech was the best performer in the first half and full year 2017).

- Both Tech and Consumer Discretionary have been the best performing U.S. sectors since 2007, with 13% and 12% annual returns respectively. Healthcare is the only other sector above 10% annual returns (barely) over the same period.

- Removing 2003 from the tables had a big negative impact on annual returns over the last 15 years. 2003 was an especially big year for several international and emerging market countries.

- A similar thing will happen to 10-year returns at the end of this year. Only it should be a big net positive (barring a worse second half), as the horrible returns of 2008 fall off. Something to keep in mind, so as not to be deceived.

Check out the updated asset class, sector, international, and emerging markets tables to compare this year so far with prior year results. Or take a copy home with you.

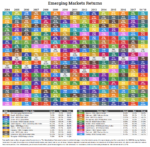

The table below includes global emerging and international market total returns, along with US sector and equity asset class total returns through 6/30/18.