Interesting things happen when market participants believe every new company will be a market leader over the next decade or two. We saw what that wild optimism looked and felt like over the last few years.

Over the three-year span, from 2019 to 2021, the S&P 500 doubled and the Nasdaq did over 1.5x better. It felt like you couldn’t lose. Yet, here we are.

Ben Graham spent a lifetime warning of the risk of eternal optimism priced into markets. Any price can be justified with enough of it:

The market action…throws an interesting sidelight on the hazards necessarily involved in buying issues on their expected future earning power. The theory that a low current rate of profit can be disregarded, provided there is strong assurance of steady future increase, has the peculiar weakness that it proves too much. For it could be used to justify any price, no matter how fantastic, merely by looking far enough ahead and making these remote profits the basis of current investment. The danger is of course that at any time the market may turn a little less far-sighted and look to the present or the near future for its measure of value.

If that doesn’t describe the market’s recent bout of optimism and the hazards incurred in 2022… And Graham wrote that in 1927!

Human nature has a perfect record in its failure to learn from past market cycles. We have a habit of takings things too far in both directions.

One risk today is that the need for quick, easy money doesn’t go away in a bear market. How many people are eyeing the prior all-time highs of last year’s biggest losers as a guide for future gains? Price decline alone does not make a stock a bargain. Especially for stocks inflated on hopes and dreams.

Value must be taken into account. Many of the companies down 80% or more had little to no value from the start. They’ll never come close to those highs again. Much like the Dotcom era, the dreams of investors far exceeded the value of the company. More importantly, some of those biggest losers still have room to fall.

The other risk may well be that investors swing too pessimistic, sell and/or avoid stocks, and miss an opportunity to put their money to work over the long run. Past market cycles have shown that investors have a habit of investing in the rearview mirror. Investors project the recent past into future expectations.

No doubt, some investors see last year’s losses as a reason to adjust their portfolio for more losses to come. The counterintuitive nature of investing suggests they do the opposite. Buying a basket of stocks at lower valuations leads to better future returns.

Besides, it’s rare for the U.S. market to experience multiple losing years in a row and international markets may be even more attractive today. Should both markets fall further, along with valuations, then those future returns only look brighter.

A note before getting to the 2022 numbers. The asset class, sector, international market, and emerging market return quilts, and the historical returns data are up-to-date. Hit the links for each one.

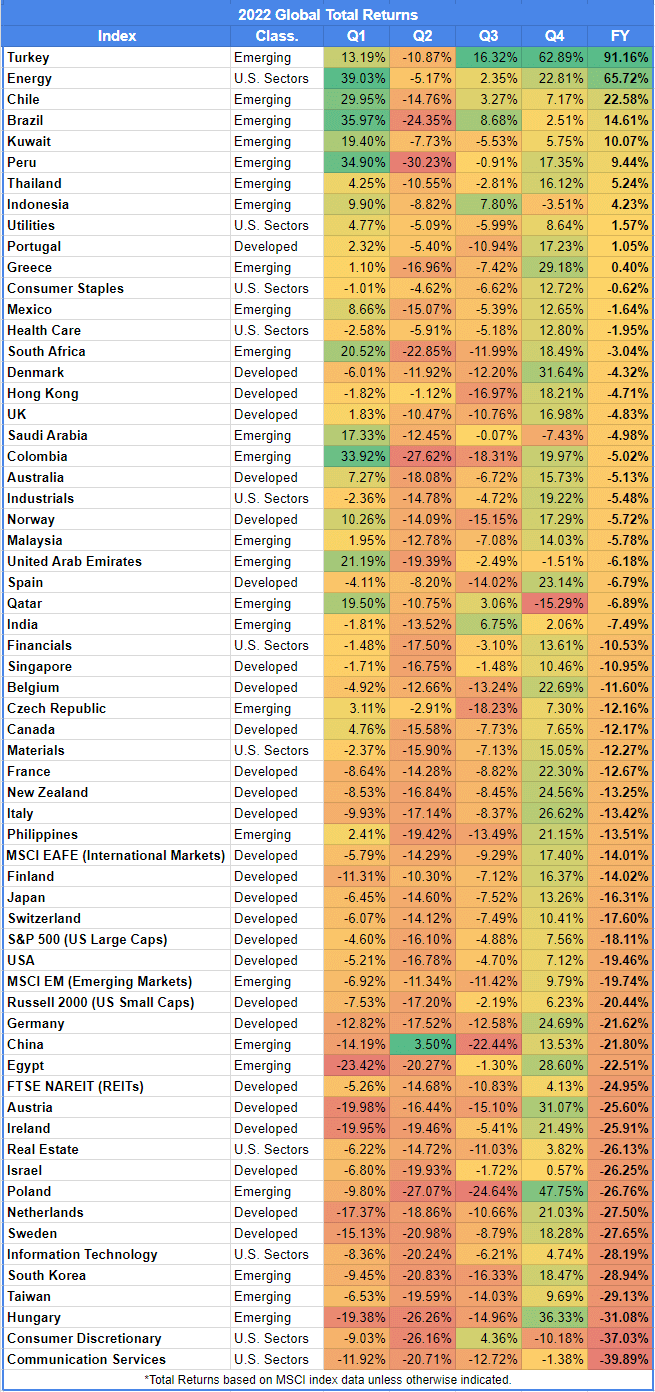

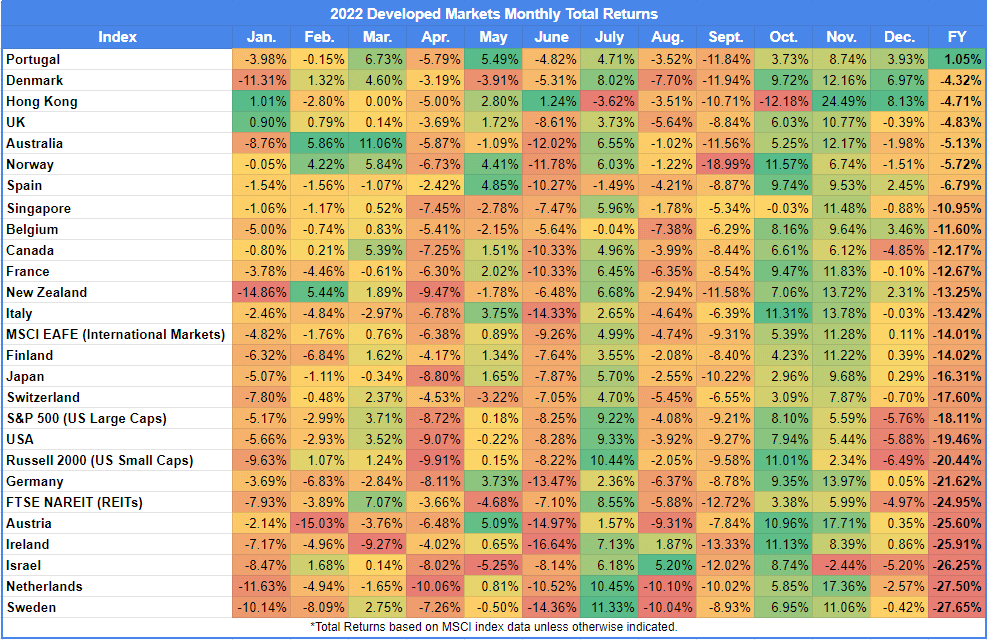

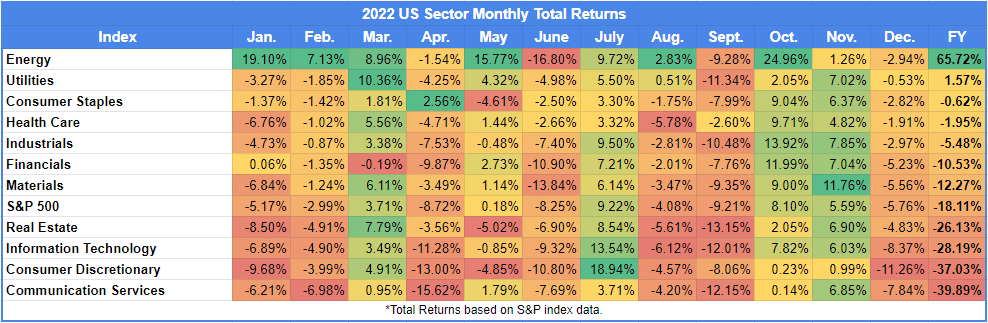

You’ll find four tables below. The first is a breakdown of the quarterly total return for global stock markets in 2022. The next three break down the total return by month for developed, emerging, and U.S. sectors respectively.

In looking at the tables, a few basic lessons should stand out:

- Annual returns are a product of wilder swings from quarter to quarter, month to month, week to week, and so on. A single number fails to relay the market fluctuations investors experience throughout any given year.

- Markets can move unexpectedly fast in both directions. Especially in bear markets. Double-digit swings both quarterly and monthly made prior years look tame by comparison. Trying to predict and time those swings with any consistency is silly.

- The advantage of diversification should be clear in the developed and emerging market tables below. Even the sector table shows how a surprisingly positive outcome in one sector can make losses more bearable for anyone who owned an S&P 500 index fund.

- The game of investing is about survival. The tables below are a reminder of the importance of risk management. Simply put, the larger the loss, the harder it is just to break even. Avoiding large losses should be top of mind around every investment decision.

And some lighter observations:

- Global markets fell in unison in the second quarter, with one exception (China). Most countries experienced double-digit losses. Peru saw the worst of it with a 30% loss.

- Global markets, practically, rose in unison in the last quarter of 2022. Only four emerging stock markets were down in the fourth quarter.

- Every developed market and emerging market was in sync in September. Losses across the board.

- Every U.S. sector saw losses in June, September, and December. Gains were had by all in July, October, and November.

- The energy sector followed up its 55% performance in 2021 with a 65.7% return on the year. It was the best performer by a landslide and one of only two — Utilities — sectors to finish in the green. It’s rare that the best-performing sector repeats two years in a row.

- The worst performing sector — Communication Services — came in at almost a 40% loss! Consumer Discretionary, Info Tech, and Real Estate sectors all performed worse than the S&P 500.

- Denmark takes the prize for the best-performing market over the last 15 years. The U.S. (S&P 500) was second, followed by Taiwan. All three exceeded a 200% cumulative return over that period.

- And the worst performer? Greece’s market index has lost 97.3% over 15 years. It needs to achieve a 3,604% return to break even. Losing big is hard to overcome. It’s one more vote for diversification.

Click the tables to enlarge.

Source:

The New Era of Discrimination in the Selection of Securities

Related Reading:

2021: A Year in Returns

2020: A Year in Returns

Last Call

- All Success is a Lagging Indicator – Ryan Holiday

- Four Wishes for 2023 – J. Zweig

- Stock Market History, Illuminated, 2022 Style – Albert Bridge

- Investment Maxims Are Not One-Size-Fits-All – Investment Talk

- FTX’s Collapse Mirrors an Infamous 18th-Century British Financial Scandal – Conversation

- Charles Ellis on the Rules of Investing (podcast) – Masters in Business

- Unlearning the Macroeconomic Lessons of the 2010s – Noahpinion

- The Most Compelling Science Graphics of 2022 – Scientific American

- Solar Panels Reduced My Electric Bill by $2,677 in 2022 – M. Bruenig