The story of markets is one of transition. Bull markets, taken to excess, lead to bear markets and back again. The first half of 2022 saw the transition to a bear market in stocks.

Yet, investors expecting their bond allocation to pick up the slack due to the decline in stocks were disappointed. Uncertainty around inflation and rising interest rates negatively hit bond prices, making it one of the worst starts to the year for both stock and bonds.

Bear markets are never enjoyable but they have some benefits. First, bear markets wash away the widespread complacency and easy money mentality in late-stage bull markets. Investing is never easy, but there are moments in the market cycle where it appears that way. Investors who confuse ease with a rising market get punished the most when the market turns.

Second, bear markets test your tolerance to drawdowns. If the performance of your portfolio makes you queasy, now is a great time to tweak your asset allocation to something you can stomach. This is especially true if this is your first bear market. Remember, you’ll never eliminate losses from your portfolio. The key is to find an asset allocation that fits your risk tolerance so you can stick to it in good times and bad.

Third, bear markets are long-term buying opportunities. Investors who diligently add new money to their portfolios every month bought stocks at lower and lower valuations over the past six months. And lower valuations lead to better returns.

The same is true for bonds. As yields on high-grade bonds almost doubled over the past six months, new money took advantage of higher yields. A simple portfolio rebalance is another way to take advantage of lower valuations and/or higher bond yields. The payoff may not seem obvious now, but it will impact returns for the better over the next decade.

Finally, the side effect of any portfolio adjustments may come in the form of tax-loss harvesting. Taxes are a drag on returns. Offsetting capital gains with capital losses in a taxable account lowers your tax burden while improving your portfolio in the process.

Of course, it’s easy to overlook the benefits when you focus on how bad markets look today. Remember that bear markets are a natural part of the market cycle that investors have faced for centuries. This one is no different. It will end like all the rest. That’s when the real benefits kicked in. Maybe seeing the current bear market in a positive light makes it easier to sit through.

A note before getting to the 2022 numbers. The asset class, sector, international markets, and emerging market return quilts are up-to-date. Hit the links for each one.

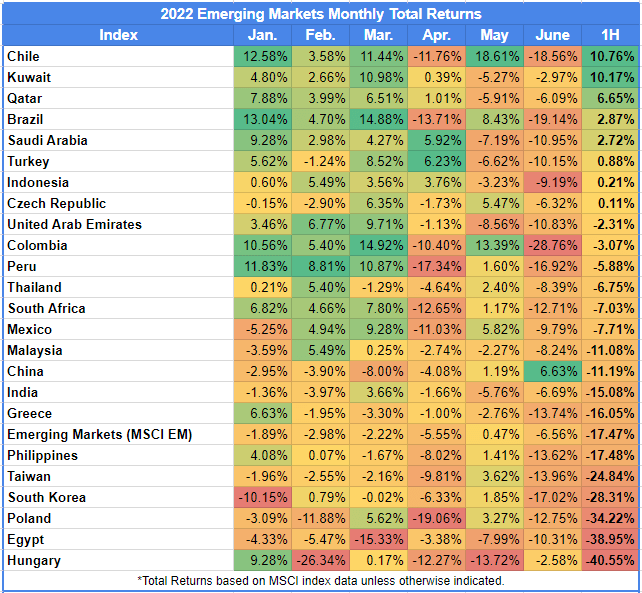

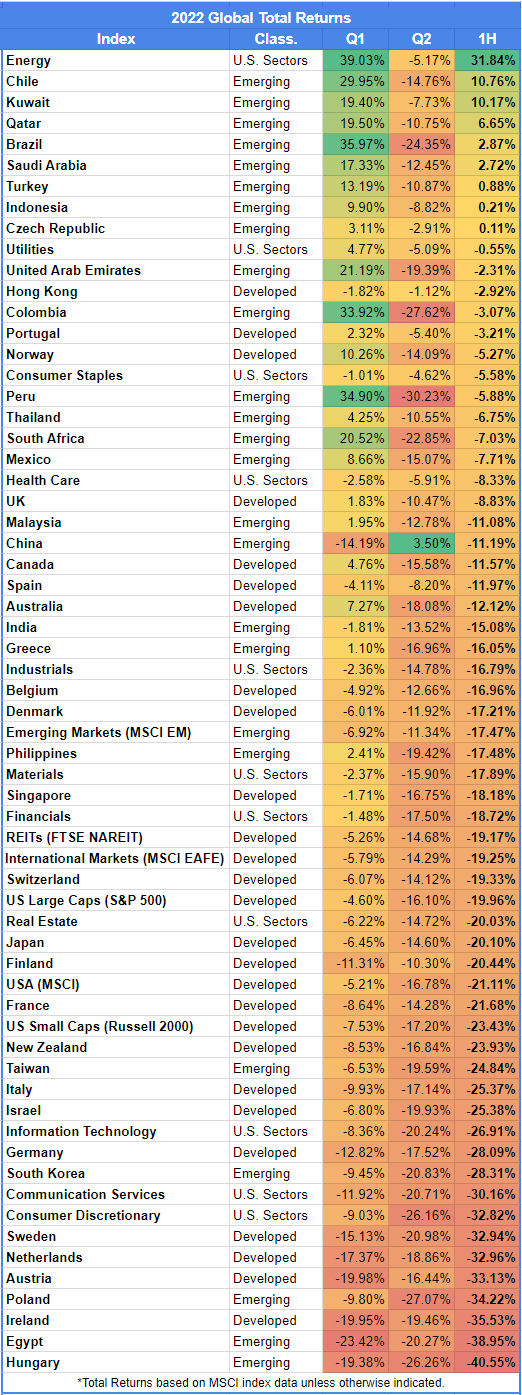

You’ll find four tables below. Each table breaks down sector, developed, and emerging markets returns by month or quarter. The charts offer a few broader lessons for investors.

- The downside of market timing should be obvious. You might get lucky and miss some big declines but will you guess correctly when to get back in for the gains? Simply being out of the U.S. stock market in the wrong month — March — would have made your overall returns worse. Or take the energy sector. Had investors dumped their money into an Energy Sector ETF in June, after the run it had from January to May, they’d be facing a 17% loss!

- Monthly and quarterly returns offer a better idea of what investors endure while earning annual returns. The last six months are proof of how difficult that can be. If anything the monthly returns show how quickly markets can fall. Some of the biggest one-month losses came in June.

- The advantages of diversification may seem overstated when stocks and bonds are falling at the same time. It’s important to note that it doesn’t happen very often. More to the point, diversification is not about eliminating losses. It spreads risk to minimize the chance of blowing up. So the average diversified portfolio may be down this year, but it’s definitely not out. That’s key to surviving bear markets.

Some lighter observations on the first half:

- Cash is king so far this year, outperforming stocks and bonds. To say that’s rare would be an understatement though.

- The energy sector picked up where it left off last year. It was not only the best performing sector but the lone bright spot to an otherwise horrid 1st half. Every other sector sat at a loss by June’s end.

- Every global developed market is down year to date — losses range from 3% to 36%.

- Emerging markets fared slightly better. Eight emerging markets are positive through six months. Hungary was the worst at a 41% loss.

- Egypt stood out as the only global market to see a loss in each month so far. Every other country had at least one positive monthly return.

- China was the only country with a second-quarter return in the green. Every other market fell in Q2. In fact, all but 7 countries saw double-digit losses in Q2. Nine of those exceeded -20% in Q2 alone.

- Finally, a side note. Three emerging market countries were downgraded by MSCI this year. Argentina, Pakistan, and Russia were removed from MSCI’s emerging market index.

Related Reading:

2021: A Year in Returns

2021: First Half Returns

Last Call

- Lifestyles – M. Housel

- Visualizing Short-Term Stock Market Performance – S. Ro

- Factor Olympics Q2 2022 – Factor Research

- Risk Capital and Markets: A Temporary Retreat or Long-Term Pull Back? – Musings on Markets

- Unexpected Inflation and Real Stock Returns – Evidence Investor

- Measuring Successful Marketing – Klement on Investing

- Are the Stocks of Stadium Sponsors Cursed? – J. Rekenthaler

- Making Microbots Smart – Knowable

- The Weird, Analog Delights of Foley Sound Effects – New Yorker