Welcome to the end of the week and another edition of Happy Hour! Just sit back, relax, and enjoy your end of the week roundup of all things interesting in the land of money.

iPad Nano

A look into the new iPad mini TV Ads show where Apple is heading. Is Apple becoming too obvious. What’s next for the iPad, iPad Mini, then iPad Nano?

In the past Apple used the software approach to its device upgrades. Just add one or two big changes each year with minor tweaks (bug fixes), call it 2.0 or 3.0 and charge its customers full price for the new product. Technology advances over the past decade made it easy as computer chips got smaller, hard drive memory grew and both got cheaper. It was an easy sell. The iPod evolution explains this concept well. It also provided a hint of where Apple was heading. First came iPod, then the iPod Mini, and finally the iPod Nano.

It may have worked for the iPod, but can you really call a smaller version of the iPad, innovative? It hasn’t introduced any mind-blowing products or upgrades in a year. Which was a regular occurrence in the past. So, has the well run dry? Or is the Apple TV its saving grace? Continue Reading…

One of the hard parts of investing is knowing when to sell once you have a profit. Another is selling too early and missing out on more profit. And, of course, through all that, you still want to protect your profit so it doesn’t become a loss. Which all sounds complicated, but a trailing stop order covers all of this and more.

One of the hard parts of investing is knowing when to sell once you have a profit. Another is selling too early and missing out on more profit. And, of course, through all that, you still want to protect your profit so it doesn’t become a loss. Which all sounds complicated, but a trailing stop order covers all of this and more. The tax code is constantly changing. Sometimes you can get a leg up on next year’s tax changes by taking advantage of any current favorable tax code.

The tax code is constantly changing. Sometimes you can get a leg up on next year’s tax changes by taking advantage of any current favorable tax code. The markets came back to reality this week. Many blamed it on the election results. Despite your political leanings, there’s been this fiscal cliff to deal with all year. And apparently Europe still has problems too. The concern going forward lies with the possible effects of expiring tax cuts. You can read all about the potential

The markets came back to reality this week. Many blamed it on the election results. Despite your political leanings, there’s been this fiscal cliff to deal with all year. And apparently Europe still has problems too. The concern going forward lies with the possible effects of expiring tax cuts. You can read all about the potential  For the past four years investors have been on a quest for higher yield as the Fed has pushed rates lower to spur economic growth. It’s been a double-edged sword. With savers being gouged by lower rates, investors have thrown risk out the window in search of higher yield. Since 2007, over

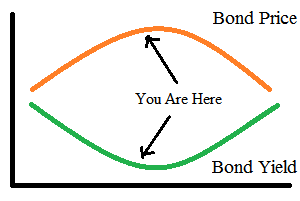

For the past four years investors have been on a quest for higher yield as the Fed has pushed rates lower to spur economic growth. It’s been a double-edged sword. With savers being gouged by lower rates, investors have thrown risk out the window in search of higher yield. Since 2007, over