Value strategies aren’t for everyone. The biggest reason is you have to do the opposite of what most investors do in order to outperform.

That’s hardly a bold statement, but after testing a number of value metrics one thing stood out. Obviously, there are benefits to buying undervalued stocks. The long-term outperformance is clear.

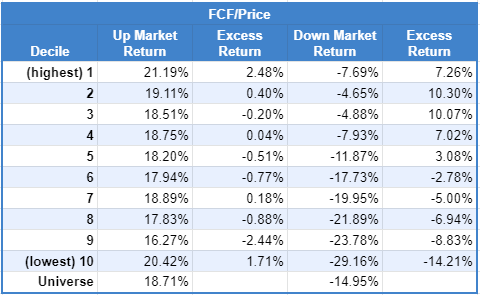

But what might surprise most people is that value’s outperformance, on average, overwhelmingly comes during down markets. Here’s an example.

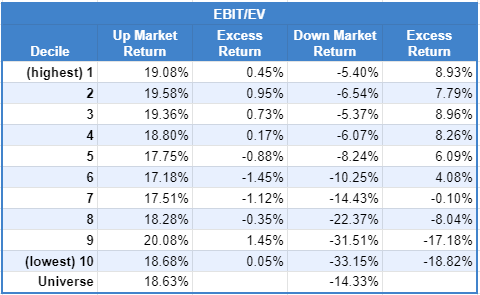

Here’s another one.

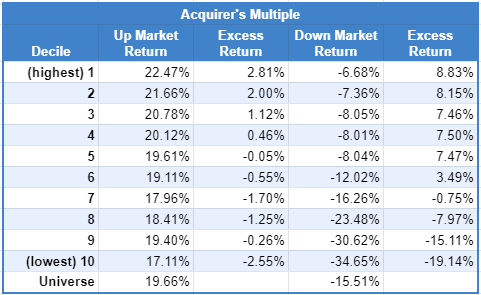

And one more.

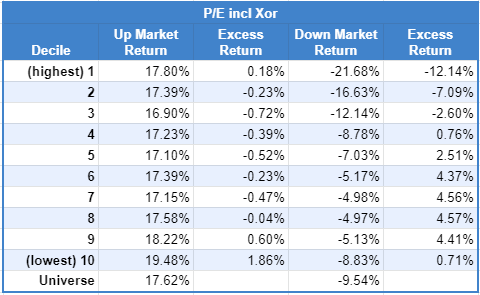

Even a simple P/E ratio follows the same pattern.

Let’s break this down. The four examples show the average excess return you would earn investing in each decile — when the market is up versus when the market is down — rather than the universe. For the top three examples, the highest decile is the cheapest stocks (for P/E, the lowest is the cheapest).

The examples follow two clear patterns. When markets are rising, value struggles to outperform, on average. Value shines when markets are down.

Value strategies are more than just buying cheap stocks. In fact, the greatest outperformance comes from buying undervalued stocks, that are getting cheaper, when the market is down.

Unfortunately, that combination flies in the face of average investor behavior. When markets are falling, most investors are preoccupied with worry. Should they sell or not fills their mind. The last thing the average investor wants to do is buy what likely appears to be a beaten-up company, fallen further in price, thanks to a correction or crash. More to the point, the average investor won’t think about buying stocks again until after the market regains its senses and starts to recover.

This behavioral pattern is so common that it likely explains why value strategies work in the first place.

Buying when the market is down is the necessary step that makes value strategies work. It’s also the hardest part for most investors to follow through on. If you can’t do that, the chance to outperform is lost. Value strategies aren’t for you.

* Note: The data can be found here, here, and here. The pattern follows on a purely quantitative basis.

Last Call

- The Most Dangerous Combination in Finance – Klement on Investing

- Great Expectations – J. Zweig

- Patient Investing is Hard – L. Swedroe

- Rumpelstiltskin and Meme Stock Investing – Albert Bridge Capital

- Always Invert – The Better Letter

- The Long Slow Short – Net Interest

- A Slow-Burning Hot Take – Tedium

- The Rise and Fall of an American Tech Giant – Atlantic

- A Battle Between a Great City and a Great Lake – NY Times